Morning Call For Nov. 13, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 +0.22%) this morning are up +0.27% at a new record high on optimism over the U.S. economic outlook and European stocks are up +0.49% on strength in technology stocks as Ericson AB rose over 3% after announcing a pan to cut costs by $1.2 billion and Illiad SA gained over 4% after reporting stronger-than-expected Q3 revenue results. Asian stocks closed mixed: Japan +1.14%, Hong Kong +0.34%, China-0.56%, Taiwan +0.69%, Australia -1.35%, Singapore +0.65%, South Korea -0.46%, India -0.24%. China's Shanghai Stock Index erased an early rally and closed lower after a person with knowledge of the talks said that China's leaders have discussed lowering the 2015 economic target below this year's target of 7.5% after today's economic data showed weaker-than-expected industrial output and retail sales. Losses in Chinese stocks were limited on the outlook for additional stimulus measures after the PBOC said it was looking to support lending to small businesses. Commodity prices are mixed. Dec crude oil (CLZ14 -0.89%) is down -0.58%. Dec gasoline (RBZ14 -1.71%) is down -1.32%. Dec gold (GCZ14 +0.28%) is up +0.15%. Dec copper (HGZ14 +0.60%) is up +0.83%. Agriculture prices are mixed. The dollar index (DXY00 -0.14%) is down -0.14%. EUR/USD (^EURUSD) is up +0.18%. USD/JPY (^USDJPY) is up +0.15%. Dec T-note prices (ZNZ14 -0.02%) are down -3 ticks.

China Oct industrial production rose +7.7% y/y, less than expectations of +8.0% y/y. Oct retail sales rose +11.5% y/y, less than expectations of +11.6% y/y and the smallest pace of increase in 8-1/2 years. Oct fixed assess investment (excluding rural households) rose +15.9% y/y, less than expectations of +16.0% y/y and the slowest pace of increase in 13-3/4 years.

The ECB Survey of Professional Forecasters cut their Eurozone 2014 GDP estimate to +0.8% from +1.0% in Aug and lowered their 2014 inflation forecast to +0.5% from +0.7% in Aug.

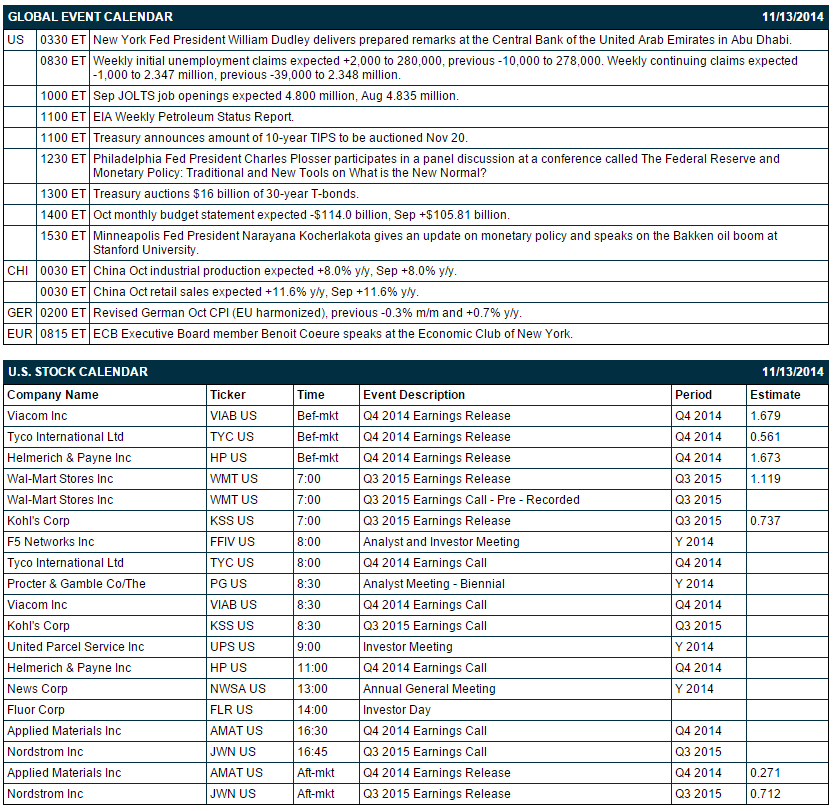

Speaking in Abu Dhabi, New York Fed President Dudley said that "the reaction of financial markets to the Fed's actions will be important in terms of how fast we go once we start to tighten monetary policy."

The UK Oct RICS house price balance was 20%, less than expectations of 25% and the lowest in 17 months.

Japan Sep industrial production was revised higher to +2.9% m/m and +0.8% y/y from the previously reported +2.7% m/m and +0.6% y/y. Sep capacity utilization rose +3.6% m/m, the strongest pace of increase in 8 months.

Japan Sep machine orders unexpectedly rose +2.9% m/m and +7.3% y/y, stronger than expectations of -1.0% m/m and -0.3% y/y.

Japan Oct PPI fell -0.8% m/m, twice the expectations of a -0.4% m/m drop and the biggest decline in 3 years. On an annual basis, Oct PPI rose +2.9% y/y, less than expectations of +3.3% y/y and the smallest pace of increase in 7 months.

U.S. STOCK PREVIEW

Today’s initial unemployment claims report is expected to show a small increase of +2,000 to 280,000 following last week’s decline of -10,000 to 278,000. Meanwhile, the market is expecting today’s continuing claims report to show a -1,000 decline to 2.347 million, adding to last week’s fairly sharp drop of -39,000 to 2.348 million. Today’s Sep JOLTS job openings report is expected to drop by -35,000 to 4.800 million, reversing part of the +230,000 surge to the 13-1/2 year high of 4.835 million seen in August. The Treasury today will sell $16 billion of 30-year T-bonds, concluding this week’s $66 billion quarterly refunding operation. There are 7 of the S&P 500 companies that report earnings today: Wal-Mart (consensus $1.12), Viacom (1.68), Tyco (0.56), Helmerich & Payne (1.67), Kohl's (0.74), Applied Materials (0.27), Nordstrom (0.71).

Equity conferences today include: Bank of America Merrill Lynch Banking & Financial Services Conference on Wed-Thu, Wells Fargo Securities Technology, Media & Telecom Conference on Wed-Thu, Goldman Sachs Global Industrials Conference on Wed-Thu, Bank of America Merrill Lynch Global Energy Conference on Wed-Fri, Edison Electric Institute Financial Conference on Thu, UBS Building & Building Products CEO Conference on Thu, SunTrust Robinson Humphrey Financial Technology, Business & Government Services on Thu, NOAH Conference 2014 on Thu, Goldman Sachs Technology and Internet Conference on Fri.

OVERNIGHT U.S. STOCK MOVERS

Wal-Mart (WMT +0.24%) climbed over 1% in pre-market trading after it reported Q3 EPS of $1.15, better than consensus of $1.12.

Viacom (VIAB -0.40%) reported Q4 EPS of $1.71, higher than consensus of $1.68.

Kohl's (KSS +2.99%) reported Q3 EPS of 70 cents, below consensus of 74 cents.

UBS reiterated its 'Buy' rating on CME Group (CME -0.80%) and raised the price target on the stock to $97 from $89.

Tyco International (TYC -0.07%) reported Q4 EPS of 56 cents, right on consensus.

UGI Corporation (UGI -1.25%) reported a Q4 adjusted EPS loss of -8 cents, a bigger loss than consensus of -5 cents.

AmeriGas (APU +0.55%) reported a Q4 EPS loss of -58 cents, a wider loss than consensus of -55 cents.

Global Brass & Copper (BRSS -1.11%) reported Q3 adjusted EPS of 51 cents, weaker than consensus of 58 cents.

WGL Holdings (WGL -0.90%) reported a Q4 EPS loss of -17 cents, a smaller loss than consensus of -26 cents, and then raised guidance on fiscal 2015 EPS to $2.70-$2.90, higher than consensus of $2.64.

Cisco (CSCO -0.16%) reported Q1 adjusted EPS of 54 cents, better than consensus of 53 cents.

J.C. Penney (JCP +7.78%) fell over 5% in after-hours trading after it reported a Q3 EPS loss of -77 cents, a smaller loss than consensus of -80 cents, but said it saw a slowdown in September and October.

NetApp (NTAP +0.09%) fell 3% in after-hours trading after it reported Q2 EPS of 70 cents, right on consensus, although Q2 revenue of $1.54 billion was below consensus of $1.55.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 +0.22%) this morning are up +5.50 points (+0.27%) at a new record high. The S&P 500 index on Wednesday closed lower: S&P 500 -0.07%, Dow Jones -0.02%, Nasdaq +0.20%. Bullish factors included (1) a decline in bank stocks after U.S, and European regulators fined five lenders a total of $3.3 billion to settle a probe into the rigging of foreign-exchange rates, (2) carry-over weakness from a slide in European equities on Eurozone growth concerns after he BOE cut its U.K. GDP and inflation forecasts, and (3) concern over escalation of the Ukraine crisis after NATO said Russia has sent columns of troops and heavy weapons into Ukraine over the past two days.

Dec 10-year T-notes (ZNZ14 -0.02%) this morning are down -3 ticks. Dec 10-year T-note futures prices on Wednesday closed higher: TYZ4 +7.00, FVZ4 +3.50. Supportive factors included (1) carry-over support from a rally in British gilts and German bunds after the BOE cut its GDP and inflation forecasts, and (2) increased safe-haven demand for T-notes after stocks fell.

The dollar index (DXY00 -0.14%) this morning is down -0.119 (-0.14%). EUR/USD (^EURUSD) is up +0.0023 (+0.18%). USD/JPY ^USDJPY) is up +0.17 (+0.15%). The dollar index on Wednesday closed higher. Closes: Dollar index +0.291 (+0.33%), EUR/USD -0.00367 (-0.29%), USD/JPY -0.285(-0.25%). Bullish factors included (1) hawkish comments from Philadelphia Fed President Plosser who said the Fed should raise rates "sooner rather than later" as that would enable them to move more gradually as data improves, and (2) weakness in stocks which boosted the safe-haven demand for the dollar. USD/JPY fell back from a 7-year high after Japanese Finance Minister Aso said that no decision has been made on postponing a national sales tax and after Japan's Chief Cabinet Secretary Suga there were no preparations for early elections.

Dec WTI crude oil (CLZ14 -0.89%) this morning is down -45 cents (-0.58%) and Dec gasoline (RBZ14 -1.71%) is down -0.0279 (-1.32%). Dec crude and Dec gasoline on Wednesday settled mixed. Closes: CLZ4 -0.76 (-0.98%), RBZ4 +0.0034 (+0.16%). Negative factors included (1) a stronger dollar, and (2) expectations for Thursday’s EIA inventory data to show crude supplies rose +1.1 million bbl and gasoline stockpiles rose +350,000 bbl. A bullish factor was the comments from Saudi Oil Minister Ali al-Naimi who said that talk of a price war within OPEC was a "misunderstanding" and that Saudi oil policy seeks steady oil prices.

Disclosure: None