Morning Call For Nov. 14, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 +0.02%) this morning are up +0.01% on increased M&A activity with Baker Hughes up over 5% in pre-market trading after it confirmed that it was in talks with Halliburton for a potential "business combination." European stocks were down -0.76 % as a slide in commodity producers outweighed economic data that showed Eurozone Q3 GDP grew more than expected. Asian stocks closed mostly higher: Japan +0.56%, Hong Kong +0.28%, China +0.05%, Taiwan +0.02%, Australia +0.21%, Singapore +0.32%, South Korea -0.77%, India +0.38%. Japan's Nikkei Stock Index rose to the highest in 7-1/4 years, led by strength in exporters, as a plunge in the yen to a 7-year low against the dollar bolstered the earnings prospects of exporters. Commodity prices are mixed. Dec crude oil (CLZ14 +0.22%) is up +0.19%. Dec gasoline (RBZ14 +0.81%) is up +0.83%. Dec gold (GCZ14 -0.70%) is down -0.86%. Dec copper (HGZ14 +0.18%) is up +0.07%. Agriculture prices are weaker. The dollar index (DXY00 +0.35%) is up +0.35%. EUR/USD (^EURUSD) is down -0.25%. USD/JPY (^USDJPY) is up +0.57% at a 7-year high on speculation Prime Minister Abe may announce a delay of a national sales tax increase and decide to dissolve parliament and call for snap elections, which are yen negative. Dec T-note prices (ZNZ14 -0.02%) are down -0.5 of a tick.

ECB Governing Council member Noyer told the French newspaper Les Echos that "inflation risks being too weak for too long" and that the ECB could begin to buy state of company debt if it decided that its policies weren't having any effect.

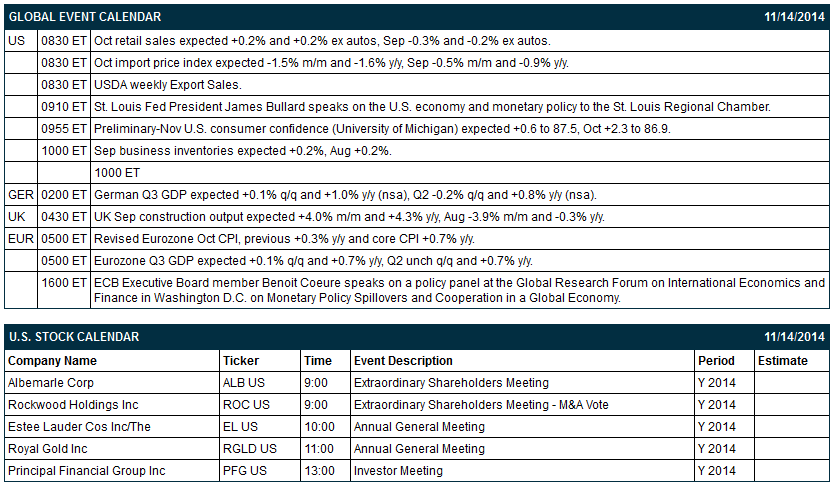

Eurozone Q3 GDP rose +0.2% q/q and +0.8% y/y, a faster pace of increase than expectations of +0.1% q/q and +0.7% y/y.

German Q3 GDP rose +0.1% q/q and +1.2% y/y (nsa), slightly stronger than expectations of +0.1% q/q and +1.0% y/y (nsa).

China Oct new yuan loans were 548.3 billion yuan, less than expectations of 626.40 billion yuan. Oct aggregate financing, China's broadest measure of credit, increased by 662.7 billion yuan, less than expectations of 887.5 billion yuan.

UK Sep construction output rose +1.8% m/m and +3.5% y/y, less than expectations of +4.0% m/m and +4.3% y/y.

U.S. STOCK PREVIEW

Today’s preliminary-Nov U.S. consumer confidence index from the University of Michigan is expected to show a +0.6 point increase of 87.5, which would be a new 7-1/3 year high. Today’s Oct retail sales report is expected to show a modest increase of +0.2% both overall and ex-autos, which would largely reverse September’s declines of -0.3% overall and -0.2% ex-autos. Today’s Oct import price index is expected to show a decline of -1.5% m/m and -1.6% y/y, which would be even weaker than the September report of -0.5% m/m and -0.9% y/y.

None of the Russell 1000 companies report earnings today. Equity conferences today include: Bank of America Merrill Lynch Global Energy Conference on Wed-Fri, Goldman Sachs Technology and Internet Conference on Fri.

OVERNIGHT U.S. STOCK MOVERS

UBS reiterates its 'Buy' rating on Best Buy (BBY +0.82%) and raised its price target on the stock to $36 from $32.

Wal-Mart (WMT +4.72%) was downgraded to 'Underperform' from 'Market Perform' at BMO Capital.

Nike (NKE +0.32%) was downgraded to 'Neutral' from 'Buy' at Sterne Agee.

TJX (TJX -0.36%) and Ross Stores (ROST -0.28%) were both downgraded to 'Sell' from 'Hold' at Canaccord.

Baker Hughes (BHI +15.24%) climbed over 5% and Halliburton (HAL +1.05%) rose over 1% in pre-market trading after Baker Hughes confirmed that "it has engaged in preliminay duscussions with Halliburton regarding a potential business combination transaction."

Harley-Davidson (HOG +0.80%) rose 1.4% in pre-market trading after Goldman Sachs upgraded the stock to 'Buy' from 'Neutral.'

Gabelli reported a 17.34% stake in Pep Boys (PBY -1.49%) .

Pennant Capital reported a 7.0% passive stake in WellCare (WCG -0.10%) .

Trinseo S.A. (TSE +1.40%) reported Q3 adjusted EPS of 1 cents, well below consensus of 14 cents.

Meritage Group reported a 5.0% passive stake in Discovery (DISCA +3.14%) .

Carter's (CRI -0.81%) was initiated with a 'Buy' at Sterne Agee with a price target of $91.

Nordstrom (JWN +0.55%) reported Q3 EPS of 73 cents, higher than consensus of 71 cents, but then lowered guidance on fiscal 2014 EPS view to $3.70-$3.75 from $3.80-$3.90, weaker than consensus of $3.86.

Applied Materials (AMAT +0.58%) slipped 3% in after-hours trading after it reported Q4 adjusted EPS of 27 cents, right on consensus, although Q4 revenue of $2.26 billion was less than consensus of $2.27 billion.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 +0.02%) this morning are up +0.25 of a point (+0.01%). The S&P 500 index on Thursday posted a new record high and closed higher: S&P 500 +0.05%, Dow Jones +0.23%, Nasdaq +0.43%. Bullish factors included (1) positive Q3 stock earnings results after Wal-Mart, Cisco and Viacom all reported better-than-expected earnings, and (2) increased M&A activity after Berkshire Hathaway bought the Duracell battery business from Procter & Gamble and after Hasbro was said to be in talks to acquire DreamWorks Animation SKG. Stocks fell back from their best levels after (1) U.S. weekly jobless claims rose +12,000 to 290,000, a larger increase than expectations of +2,000 to 280,000, and (2) energy producers declined as the price of crude oil tumbled to a 4-year low.

Dec 10-year T-notes (ZNZ14 -0.02%) this morning are down -0.5 of a tick. Dec 10-year T-note futures prices on Wednesday closed higher: TYZ4 +5.00, FVZ4 +3.50. Bullish factors included (1) the larger-than-expected increase in U.S. weekly initial unemployment claims, and (2) short-covering by bond dealers after the Treasury concluded this week’s $66 billion of Treasury auctions with the sale of $16 billion of 30-year T-bonds.

The dollar index (DXY00 +0.35%) this morning is up +0.307 (+0.35%). EUR/USD (^EURUSD) is down -0.0031 (-0.25%). USD/JPY (^USDJPY) is up +0.66 (+0.57%) at a new 7-year high. The dollar index on Thursday closed lower. Closes: Dollar index -0.148 (-0.17%), EUR/USD +0.0038 (+0.03%), USD/JPY +0.28 (+0.24%). Bearish factors included (1) comments from New York Fed President Dudley who said that raising interest rates too early poses a bigger risk to the economy than acting too late, and (2) the larger-than-expected increase in U.S. weekly jobless claims.

Dec WTI crude oil (CLZ14 +0.22%) this morning is up +14 cents (+0.19%) and Dec gasoline (RBZ14 +0.81%) is up +0.0166 (+0.83%). Dec crude and Dec gasoline on Thursday closed sharply lower with Dec crude and Dec gasoline at 4-year lows. Closes: CLZ4 -2.97 (-3.85%), RBZ4 -0.1054 (-5.00%). Bearish factors included (1) the +1.7 million bbl increase in crude inventories at Cushing, OK, the delivery point of WTI futures, to a 5-1/2 month high of 22.5 million bbl, and (2) the +1.0% increase in U.S. crude production in the week ended Nov 7 to 9.063 million bpd, the most in 40 years.

Disclosure: None