5 Big Name Stocks That Remain Good Values

Guest Post by Michael Fowlkes

The word "expensive" is a rather relative term. What is expensive to me may not be to you, and at the same time what is expensive to you may appear cheap to your neighbor. In most aspects of life, whether or not something is expensive depends a lot on your financial status.

However, when it comes to investing, this is not exactly the way things work out. While it is in our human nature to judge a security as expensive or inexpensive based on its stock price, simple stock price is actually the worst way to assign a value to a stock. In some cases, stocks that trade over $100 a share are actually very good values, while some stocks trading under $10 present horrible value to investors.

There are various ways to assign value to stocks, but the one I fall back on the most is a stock's price-to-earnings ratio, also known as the P/E ratio. The P/E ratio looks at the stock price in relation to the company's earnings, which is a fair way to determine whether or not the stock is trading in overbought or undersold territory.

Everyone has their own opinion on what P/E suggests a fairly valued stock, but from my point of view, I consider stocks trading with a P/E in a range of 15 to 20 being fairly valued, and once the P/E rises above that range the security is starting to look a bit pricey. However, you also need to take into consideration where other stocks in the same industry are trading as well.

This week we are going to look at a handful of stocks that appear expensive at first glance, which actually offer decent value to investors at the current time.

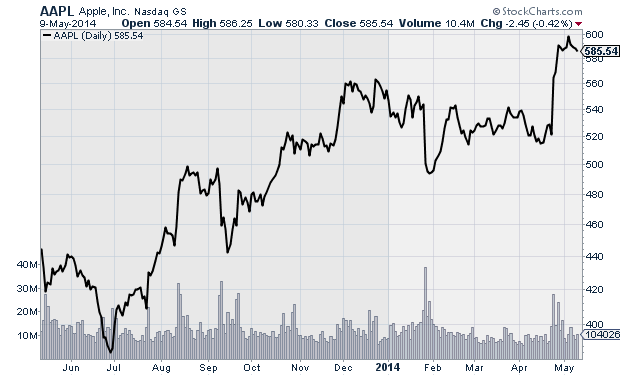

Apple (AAPL)

Tech giant Apple (AAPL) is the easy example. With the stock currently trading slightly above $585, it is natural to jump to the conclusion that it is a very expensive stock. It may be a fair assumption, since we do not often see stocks trading at such a lofty price, but Apple's P/E ratio is actually rather small, at just 14, which is basically in-line with Microsoft's (MSFT) P/E of 14.8, more attractive that tech-heavyweight Google's (GOOG) P/E of 27. When compared to these two other tech giants, Apple starts to look much more affordable, but if the $585 price tag still turns you off, you are in luck since the company recently announced plans to split its stock 7:1, so psychologically the stock is about to look a lot cheaper. Also consider that Wall Street expects the company to grow earnings by 9% in 2015 vs. 2014.

AAPL Chart

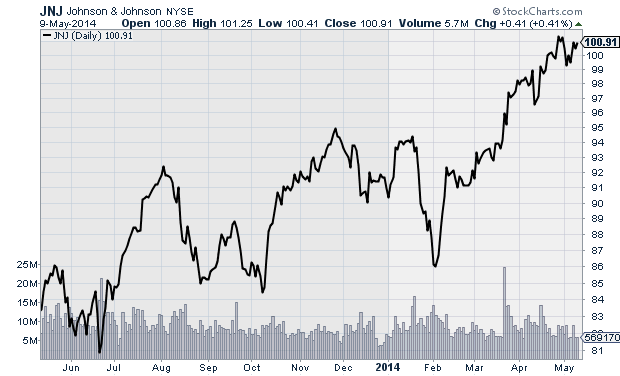

Johnson & Johnson (JNJ)

Drug manufacturer and consumer healthcare product heavyweight Johnson & Johnson (JNJ) was trading in the upper $60's at the start of 2013, but after a year and a half of strong gains, it is currently trading at $100.91 a share. With the stock crossing through the psychological $100 barrier, it would be easy to have a knee-jerk reaction to the stock with the assumption that the stock has entered overbought territory. However, taking a closer look, the stock does not really appear to be all that expensive, as it trades with a P/E of just 19.3. While that is on the upper end of my comfort range, it is still not too high to consider expensive at the current time. On the pharmaceutical side, we can compare JNJ with Merck (MRK), which has a P/E of 36. On the consumer products side, we can compare the company to Procter & Gamble (PG), which trades with a P/E of 22. In both instances, JNJ appears to be a good value at its current level. Looking ahead, Wall Street believe that the company is going to grow its earnings by 8% next year, which should keep support under the stock.

JNJ Chart

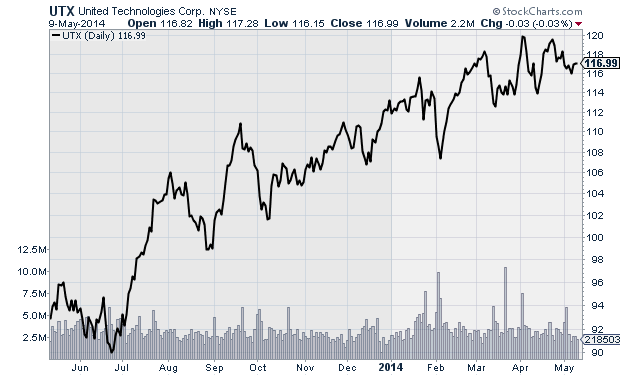

United Technologies (UTX)

Aerospace and defense services provider United Technologies (UTX) has a current stock price of $116.99, but has a price-to-earnings ratio of 18.9. Over the last two years the stock has been moving steadily higher, but even with UTX currently trading just shy of its 52-week high, there still appears to be value left in the stock. UTX's P/E ratio does not raise any red flags as far as the stock being overbought; when compared with some of its competitors the stock looks even more affordable. One of the better companies to compare UTX to is Boeing (BA), which currently has a P/E ratio of 22.6. Don't let the high price tag and recent stock strength fool you, UTX is fairly valued, and still has additional upside potential, as Wall Street has forecast 11% earnings growth next year.

UTX Chart

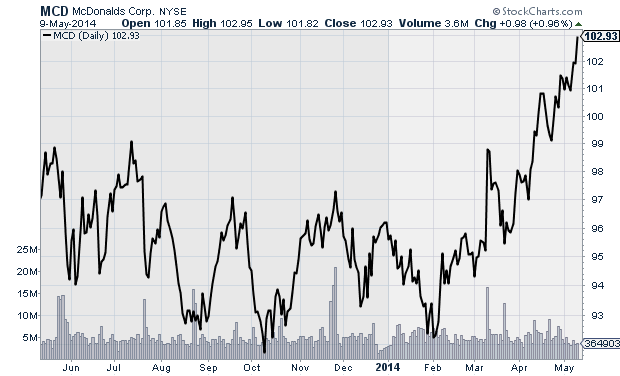

McDonald's (MCD)

Fast food heavyweight McDonald's (MCD) has received its fair share of criticism in recent years, as consumer appetites have shifted towards "healthier" fast food options, but the stock has roared back to life over the last couple of months and is currently trading just pennies below its 52-week high at $102.93. Anytime a stock crosses above the psychological $100 level, our brains try to trick us into believing it has become too expensive, but in MCD's case, the stock is trading more attractively than other companies in its industry. We could compare the stock with the likes of Chipotle Mexican Grill (CMG), which has a P/E of 47, or Panera Bread (PNRA) with a P/E of 23, but those comparisons are not the best since these two companies are part of the healthier sector of fast food that Wall Street loves. A better comparison would be against Wendy's (WEN), which has a P/E of 38. When compared to any of the three, McDonald's look like a good value, even with the stock trading at its 52-week high. Even with the concern over America's shifting appetite, analysts have forecast 11% earnings growth next year, which should keep the stock trading in the right direction.

MCD Chart

AutoZone (AZO)

At first glance, auto parts retailer AutoZone (AZO) seems to be very expensive, with a stock price of $535.92, and trading less than 5% below its 52-week high. However, despite the big price tag, it does appear to be a better value than its biggest competitors. AZO has a price-to-earnings ratio of 18, which is lower than both Advance Auto Parts (AAP), which has a P/E of 23.4, and Pep Boys (PBY) which trades with a P/E of 80. Based on these comparisons, AZO appears to be a good value even at its current price. Wall Street expects solid earnings growth of 13% in 2015, which will help keep push the stock even higher than its current level.

AZO Chart

Disclosure: None.