Rates Spark: Pushing Back

The main cues for rates markets this week and next will come from central banks. The ECB meets this Thursday, the Fed and BoE in short order next week. The persistent inflation scare is seeing expectations tilt towards tighter policies, and any pushback by the ECB may remain confined to the very front-end pricing.

Image Source: Unsplash

Final cues set the stage for upcoming central bank meetings

The European Central Bank and Fed are already in their quiet periods, while the Bank of England’s Tenreyro was the last to speak ahead of next week’s meeting. Being a known dove she spoke out for waiting on hiking the base rate. While front-end Gilt yields traded marginally lower, it was Bunds that led a front-end rally yesterday. Admittedly, EUR rates is where the discrepancy between market pricing and current official communication including the forward guidance is probably the largest just ahead of this week’s ECB meeting. And EUR rates are coping to a larger degree with a slowing growth dynamic, again confirmed by the fourth consecutive slide of the German Ifo index yesterday. (FXE)

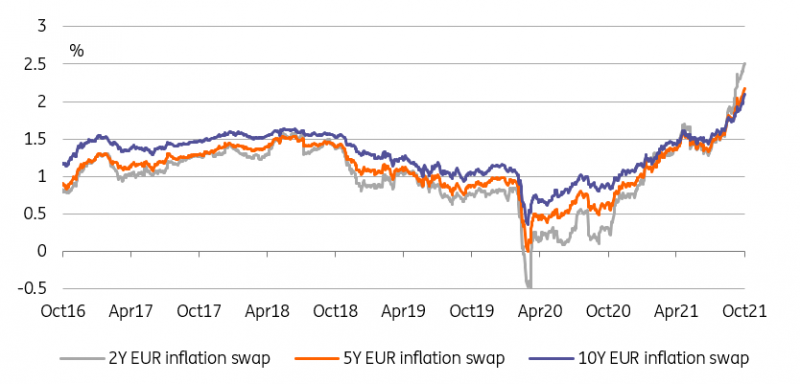

Rising inflation swaps will be a key topic at Thursday's ECB meeting

Source: Refinitiv, ING

The inflation scare will continue to tilt expectations toward tighter policies

That said, in the grander picture yesterday’s rebound was miniscule. What remains front and centre to market concerns is the inflation outlook, and there appears no end in sight to the scare with more data due this week to fuel it. The 5y5y EUR inflation swap has just climbed a further 10bp above 2% after just having straddled that mark at the end of last week. Pricing in more policy tightening seems the right response. But particularly in EUR, we have some qualms with the form the expected tightening is currently taking on, being too narrowly focussed on pulling forward rate hikes and seemingly brushing aside the implications this should have on the ECB purchase programmes. Current ECB guidance still sees them ending before any rate hikes.

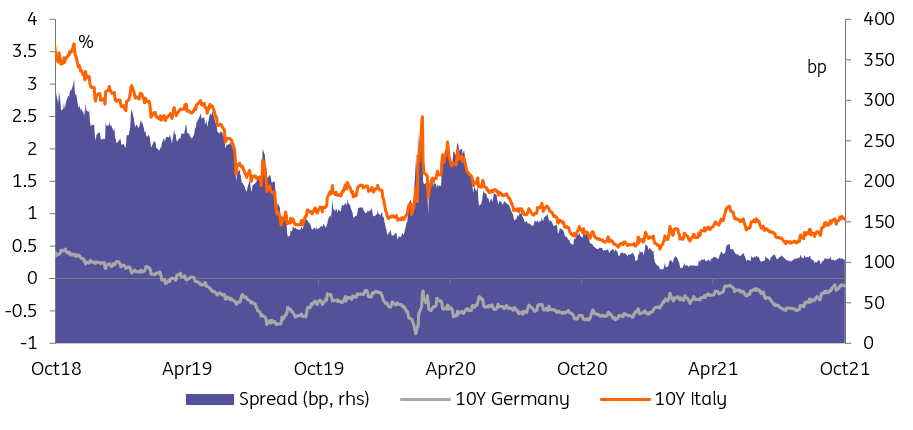

Fiscal transfers can only shield Italian bonds for so long against the withdrawal of ECB support

Source:Refinitiv, ING

Sovereign spreads are likely the most vulnerable should there be any shift in focus towards any larger-than-anticipated scaling down of ECB purchase programmes – in size or flexibility. Currently, key spreads such as the 10Y Italy/Bund spread have proven remarkably stable despite increased policy tightening angst. One reason that will have dampened the impact is of course the substantial recovery aid extended by the EU and reforms that have been kicked off. But even S&P, which raised the outlook of Italy’s BBB rating from stable to positive, remarks that part of that improved outlook is backed by the ECB's outsized support during the pandemic, something which should not be taken for granted.

Today’s events and market view

Technical factors should still prove supportive for EUR rates going into month-end before the ECB meeting is likely to stir things up. Long end rates could remain focussed on the discussion of rising inflationary risks, while reaction to a selective pushback against current front-end pricing could remain confined to just there. In all it may still be sufficient to see EUR rates outperform versus the US for instance.

Today’s calendar is relatively light with Conference Board consumer confidence and housing data out of the US in the spotlight.

In supply, the Netherlands taps its 10Y while Germany reopens the 7Y. Italy is active in reopening a 30Y inflation linked bond as well as 3Y nominal bond.

Disclaimer: Riki nema disclaimer.

Comments

No Thumbs up yet!

No Thumbs up yet!