What To Do About The “Crazy Euro”?

From today’s FT:

ECB under pressure to tackle ‘crazy’ euro

Pressure is mounting on the European Central Bank to take action against a persistently strong euro with a leading industrialist calling on Frankfurt to tackle the “crazy” strength of the currency.

…

Fabrice Brégier, chief executive of Airbus’s passenger jet business, said the ECB should intervene to push the value of the euro against the dollar down by 10 per cent from an “excessive” $1.35 to between $1.20 and $1.25.

…

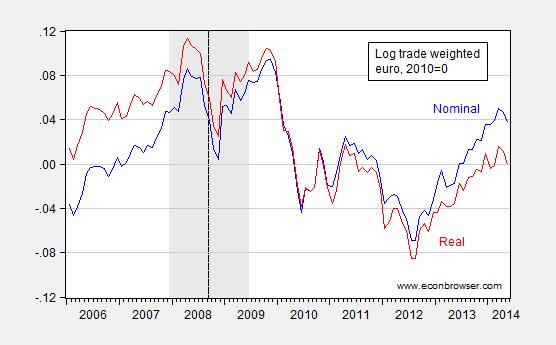

Following the euro over time, it’s clear that the euro is fairly strong, although not matching the levels in period just around the financial crisis. Remember, however, the dollar was particularly weak — and hence the euro particularly strong — just before the onset of the recession.

Figure 1: Log trade weighted value of the euro (broad), nominal (blue) and real (red), 2010=0. NBER defined US recession dates shaded gray. Dashed line at Lehman bankruptcy. Source: BIS.

Still, with euro area growth just barely creeping into the positive area, and with inflation far below target range, one could easily see how a weaker euro could help on both counts.

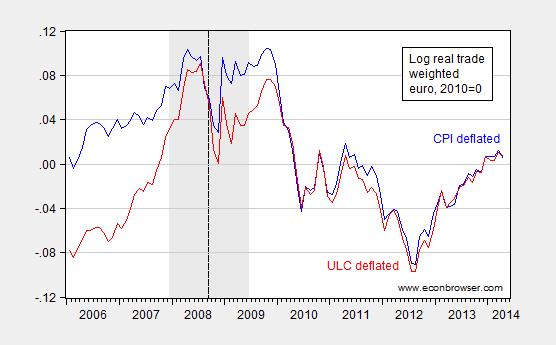

In terms of competitiveness, one would want to look to the unit labor cost deflated measures, rather than the CPI-deflated measure. Here, the same pattern emerges.

Figure 2: Log CPI-deflated trade weighted value of the euro (blue), and relative unit labor cost deflated (red), 2010=0. NBER defined US recession dates shaded gray. Dashed line at Lehman bankruptcy. Source: IMF IFS.

In the past, I (along with Jeff Frieden) have urged an increase in inflation. We didn’t post a mechanism for achieving that higher inflation, although the usual unconventional monetary policy measures — including credit easing– would have been in contention. However, increasing the ECB’s balance sheet faces some difficulties, ranging from legal to operational.

Nonetheless, today’s headline reminded me of Jeff Frankel’s proposal, made back in March.

The ECB should further ease monetary policy. Inflation at 0.8% across the Eurozone is below the target of ‘close to 2%’, and unemployment in most countries is still high. Under the current conditions, it is hard for the periphery countries to bring their costs the rest of the way back down to internationally competitive levels as they need to do. If inflation is below 1% Eurozone-wide, then the periphery countries have to suffer painful deflation.

The question is how the ECB can ease, since short-term interest rates are already close to zero.

…

What, then, should the ECB buy, if it is to expand the monetary base? It should not buy euro securities, but rather US treasury securities. In other words, it should go back to intervening in the foreign exchange market. Here are several reasons why.

First, it solves the problem of what to buy without raising legal obstacles. Operations in the foreign exchange market are well within the remit of the ECB.

Second, they also do not pose moral hazard issues (unless one thinks of the long-term moral hazard that the ‘exorbitant privilege’ of printing the world’s international currency creates for US fiscal policy).

Third, ECB purchases of dollars would help push the foreign exchange value of the euro down against the dollar.

…

Disclosure: None.