Q2 Earnings Season Off To A Solid Start Despite Recession Fears

- For the 60 S&P 500 companies that have reported Q2 results, total earnings are down -11% from the year-earlier period on +6.6% higher revenues, with 73.3% beating EPS estimates and 63.3% beating revenue estimates.

- The drag from the Finance sector accounts for most of the earnings decline, with the year-over-year growth pace improving to +12% for the companies that have reported when the Finance sector is excluded from the numbers.

- Tough comparisons to the year-earlier period that was boosted by big reserve releases is the primary reason for the Finance sector’s -27% year-over-year earnings decline. Excluding the impact of reserves, Q2 earnings would be essentially flat from the year-ago period as declines in investment banking and mortgages were offset by net interest income and trading gains.

- The overall picture emerging from the Q2 earnings season at this admittedly early stage is inconsistent with an economy heading into a significant downturn.

At this stage in the Q2 earnings season, with about 12% of S&P 500 results already in, we are simply not seeing anything that would be consistent with the all-around market worries about an imminent economic slowdown or even a recession.

Granted some companies have guided lower, as we have cited Nike (NKE), Lennar (LEN) and others, but there are many others that have either reiterated earlier guidance or actually upgraded their outlook.

Take for example the Financials whose headline Q2 earnings growth is the weakest of all the major sectors as a result of tough comparisons. We saw all the major banks, including the likes of JPMorgan (JPM Quick QuoteJPM - Free Report) talk up the outlook for households and businesses, even as they acknowledged that the growth pace should moderate over time as a result of the aggressive Fed posture.

Simply put, the picture emerging from the Q2 earnings season is inconsistent with the U.S. economy heading into a major economic downturn.

This suggests that we will likely need to wait some more, perhaps until the Q3 reporting cycle in October, to get clarity on the revisions question. That said, we have had some estimate cuts already, though they are nowhere near what would be consistent with a significant economic slowdown, not to mention a recession.

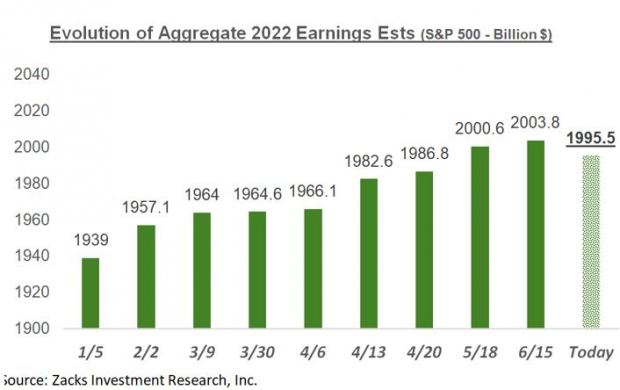

You can see in the chart below that the aggregate earnings total for this year has actually increased since the start of the year.

Image Source: Zacks Investment Research

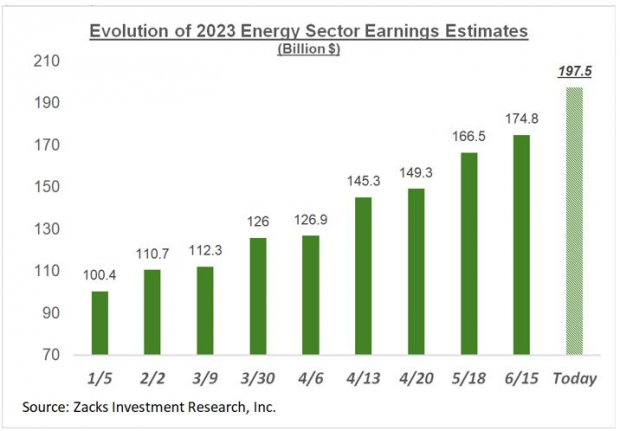

A very big part of the above positive revisions trend is thanks to the Energy sector, which you can see below.

Image Source: Zacks Investment Research

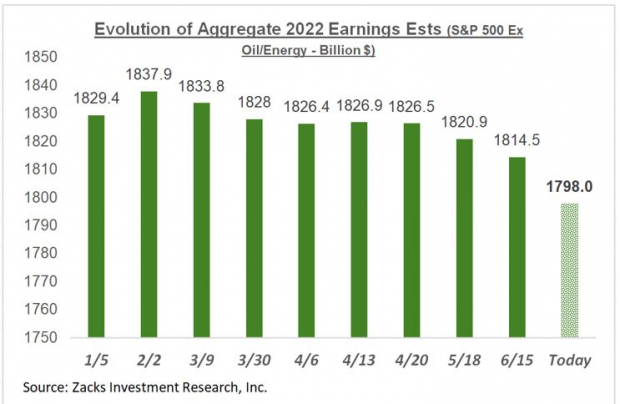

The chart below shows us the aggregate revisions trend for the S&P 500 index on an ex-Energy basis.

Image Source: Zacks Investment Research

As you can see above, aggregate S&P 500 earnings outside of the Energy sector have declined -1.7% since the start of the year, with double-digit percentage declines in the Consumer Discretionary (down -15.6%), Retail (-14.1%) and Aerospace (-16.6%) sectors.

Aggregate Energy sector earnings estimates for the year have increased by +80.2% since the start of the year. Other sectors enjoying significant positive revisions since the start of the year include Basic Materials, Autos, Consumer Staples and Construction.

A lot will be riding on how management teams share evolving business trends in their industries on the Q2 earnings calls. But given the lag with which tighter monetary policy seeps through to the broader economy, we may have to wait some more to get greater clarity.

The Overall Earnings Picture

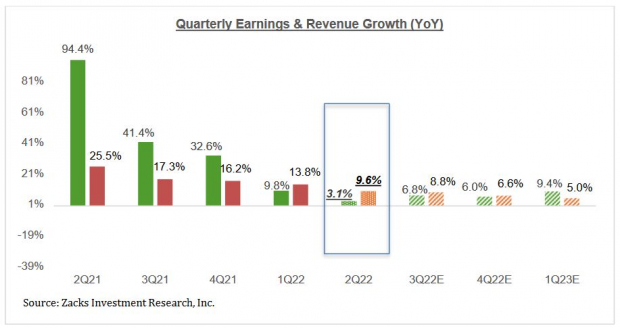

Beyond Q2, the growth picture is expected to modestly improve, as you can see in the chart below that provides a big-picture view of earnings on a quarterly basis.

Image Source: Zacks Investment Research

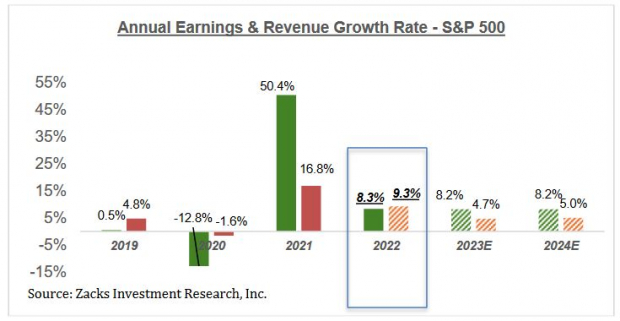

The chart below shows the overall earnings picture on an annual basis, with the growth momentum expected to continue.

Image Source: Zacks Investment Research

As strong as the full-year 2022 earnings growth picture is expected to be, it’s worth remembering that a big part of it is due to the unprecedented Energy sector momentum. Excluding the Energy sector, full-year 2022 earnings growth for the remainder of the index drops to only +2.5%.

There is a rising degree of uncertainty about the outlook, reflecting a lack of macroeconomic visibility in a backdrop of Fed monetary policy tightening. The evolving earnings revisions trend will reflect this macro backdrop.

More By This Author:

test

fwefawe

tetwet

test

1

good!

good

SASASASA

Loading comments, please wait...