BEA Revises 3rd Quarter 2014 GDP Growth Upwards To 3.89% Annualized Rate

In their second estimate of the US GDP for the third quarter of 2014, the Bureau of Economic Analysis (BEA) reported that the economy was growing at a +3.89% annualized rate, up +0.35% from their first estimate for the 3rd quarter but still down some -0.70% from the 4.59% annualized growth rate registered during the second quarter.

The modest improvement in the headline number masks substantial changes in the reported sources of the annualized growth. The previously reported significant inventory draw-down almost vanished completely (dropping to a mere -0.12% impact on the headline number). Improving fixed investments added +0.23% to the headline, with nearly all of that improvement from spending for commercial equipment. Consumer spending for goods was also reported to be growing about a quarter of a percent faster (+0.27%) in this report, while consumer spending for services was essentially unchanged (+0.02%).

Offsetting those upside revisions was a significant erosion in the previously reported export growth, which subtracted -0.38% from the headline. The contribution from imports in the headline number also weakened, taking the annualized growth down another -0.17%. Governmental spending was also revised down slightly, knocking another -0.07% from the headline. Nearly all of that downward revision to governmental spending was from reduced state and local investment in infrastructure.

Despite the increased consumer spending, households actually took a disposable income hit in this revision -- losing $146 in annualized per capita disposable income (now reported to be $37,525 per annum). This is down $344 per year from the 4th quarter of 2012. The spending growth reported above came exclusively from reduced household savings, which dropped a full half percent in this report.

As mentioned last month, softening energy prices play a major role in this report, since during the 3rd quarter dollar-based energy prices were plunging (and have continued their dive since). US "at the pump" gasoline prices fell from $3.68 per gallon to $3.32 during the quarter, a 9.8% quarter-to-quarter decline and a -33.8% annualized rate -- pushing most consumer oriented inflation indexes into negative territory. During the third quarter (i.e., from July through September) the seasonally adjusted CPI-U index published by the Bureau of Labor Statistics (BLS) was actually mildly dis-inflationary at a -0.10% (annualized) rate, and the price index reported by the Billion Prices Project (BPP -- which arguably reflected the real experiences of American households) was slightly more dis-inflationary at -0.18% (annualized).

Yet for this report the BEA effectively assumed a positive annualized quarterly inflation of 1.40%. Over reported inflation will result in a more pessimistic growth data, and if the BEA's numbers were corrected for inflation using the appropriate BLS CPI-U and PPI indexes the economy would be reported to be growing at a spectacular 5.42% annualized rate. If we were to use just the BPP data to adjust for inflation, the quarter's growth rate would have been an astounding 5.52% annualized rate.

Among the notable items in the report :

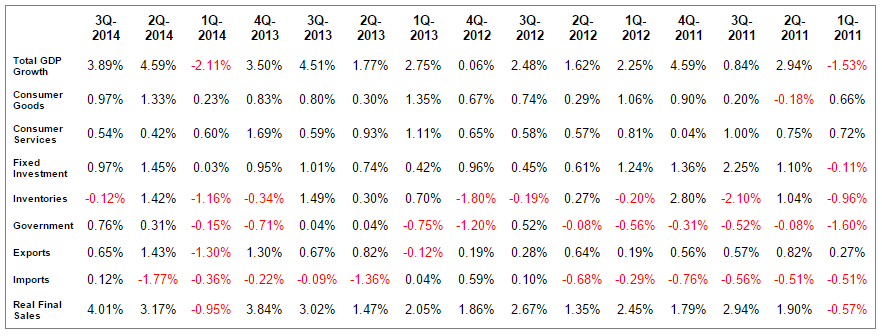

-- The headline contribution of consumer expenditures for goods was 0.97% (up +0.27% from the previous estimate, but down -0.36% from the prior quarter).

-- The contribution made by consumer services spending increased to 0.54% (up +0.02 from the previous report and +0.12% from the 0.42% reported last quarter). The combined consumer contribution to the headline number by consumers was 1.51%, down -0.24% from the prior quarter.

-- Commercial private fixed investments provided +0.97% of the headline number (down -0.48% from the 1.45% in the 2nd quarter), and this continued positive growth is nearly all non-residential.

-- Inventories subtracted only -0.12% from the headline number (up +0.45% from the -0.57% previously reported).

-- Governmental spending added +0.76% to the headline. The improvement was nearly all at a Federal level, in spending on "consumption expenditures". The growth of state and local spending softened -0.29% relative to the 2nd quarter. The growth in Federal spending was likely spending pulled forward from the 4th quarter as a result of fiscal year-end budgetary maneuvers -- and is therefore also likely to reverse in 4Q-2014.

-- Exports are now reported to be adding 0.65% to the headline growth rate (down -0.38% from the first estimate and -0.78% from the second quarter).

-- Imports added +0.12% to the headline number (down -0.17% from the previous estimate, but up +1.89% from the prior quarter). The combined revisions in the foreign trade data removed over a half percent from the previous estimate's headline.

-- The annualized growth rate for the "real final sales of domestic product" is now reported to be 4.01% (down -0.10% from the previous report). This is the BEA's "bottom line" measurement of the economy, and it is slightly higher than the headline number because of the mildly shrinking inventories.

-- And as mentioned above, real per-capita annual disposable income was revised downward by $146 per year, halving the previously reported quarter-to-quarter increase. The new number represents an annualized growth rate of 1.56%. Real disposable income is still down a material -$344 per year from the fourth quarter of 2012 (before the FICA rates normalized) and it is up only 2.31% in total since the second quarter of 2008 -- a miserable 0.37% annualized growth rate over the past 6 and a quarter years.

The Numbers, As Revised

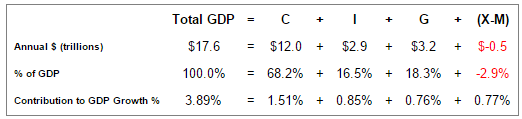

As a quick reminder, the classic definition of the GDP can be summarized with the following equation :

GDP = private consumption + gross private investment + government spending + (exports - imports)

or, as it is commonly expressed in algebraic shorthand :

GDP = C + I + G + (X-M)

In the new report the values for that equation (total dollars, percentage of the total GDP, and contribution to the final percentage growth number) are as follows :

GDP Components Table

The quarter-to-quarter changes in the contributions that various components make to the overall GDP can be best understood from the table below, which breaks out the component contributions in more detail and over time. In the table below we have split the "C" component into goods and services, split the "I" component into fixed investment and inventories, separated exports from imports, added a line for the BEA's "Real Final Sales of Domestic Product" and listed the quarters in columns with the most current to the left :

Quarterly Changes in % Contributions to GDP

Summary and Commentary

There are a number of pros and cons in this revision:

-- As mentioned last month, at face value these kinds of growth numbers arguably strengthen the Fed's rationale to extricate itself from unconventional forms of stimulus. An economy that is reported to be growing at 3.89% is presumably healthy enough to need very little additional help from central banking officials.

-- Rapidly changing dollar-based commodity prices (and more specifically energy prices) are likely playing havoc with both the BEA's inventory and net import/export data, both of which changed materially in this revision. While one might expect inventories to be valued exclusively using some variation of book-value FIFO accounting logic, they are in fact additionally impacted by an "inventory valuation adjustment" (or "IVA") that utilizes price changes from a "Fisher formula" (that according to the BEA's notes "incorporates weights from two adjacent quarters; quarterly indexes are adjusted for consistency to the annual indexes before percent changes are calculated") when converting inventory values from "nominal" to "real". For this reason rapidly changing dollar based price levels can cause "real" inventories and net import/export data to fluctuate even if physical quantities remain relatively constant -- providing temporary "noise" that duly reverses in subsequent quarters.

-- From a global perspective, this reported growth is extraordinary. Again at face value, this report shows an economy isolated (if not benefiting through falling dollar-based commodity prices) from softening global economies.

-- That said, consumers are not spending as if the US economy is healthy and sustainable. Consumers generated well less than half of the headline growth even though they are still over two-thirds of the economy. And half of the previously reported growth in real per-capita disposable income vanished in this revision -- explaining to some extent why consumers have remained wary.

-- The impact of falling energy prices will certainly carry forward into the fourth quarter. The $.36 per gallon drop in "at-the-pump" prices for gasoline during the 3rd quarter alone should have freed up over $50 billion in annualized consumer cash -- transforming it from non-discretionary spending into leftover "pocket money." And since September 30th gasoline prices have dropped another $.52, adding an additional $73 billion annualized to those pockets. Total aggregate discretionary pocket cash available to households in the 4th quarter could amount to as much as 3% of total annualized consumer goods spending.

-- What then happens to that free cash is critical to the economy. If consumers are in a mood to spend, the money will flow into record discretionary holiday sales -- even if from a GDP standpoint that incremental holiday spending is actually a zero sum exercise (savings at the non-discretionary pump simply transferred into much hyped discretionary holiday retail sales). But the kicker is simply this: if consumers remain wary, net savings could increase even further and total consumer spending (discretionary and non-discretionary) might actually decrease.

We are likely living an ancient Chinese curse: the fourth quarter should, at the very least, be "interesting."

Comments

No Thumbs up yet!

No Thumbs up yet!