Concerning Doji Bar Amid All-Time Highs – Weekly Market Outlook

Although the market didn't go anywhere during the latter half of last week, Tuesday's surge – fueled by the lack of military action in Ukraine – was big enough to more than offset Monday's loss and the inaction seen after Tuesday. Better still, there was a subtle clue given last week that says the bigger undertow is still bullish.

We'll look at that clue in a second. First, let's dissect last week's economic numbers.

Economic Calendar

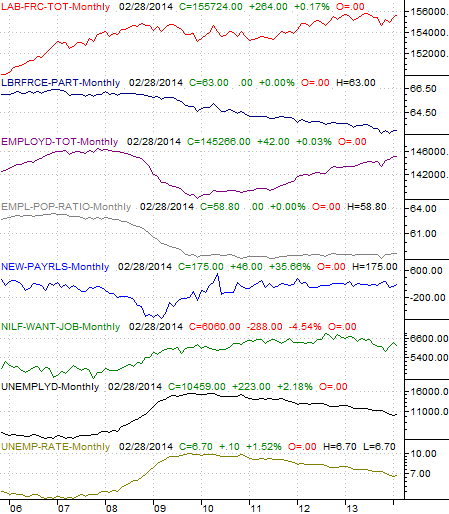

The big data last week was February's employment information. Last month, the nation added 175,000 new jobs, though the unemployment rate was ratcheted up from 6.6% to 6.7%. How's that happen? Because more than 175,000 people put themselves back into the labor force, and there weren't enough jobs for all them. Still, though not red hot, the jobs situation once again got a tad better.

Employment Snapshot Chart

Underscoring that modest improvement in the job market is the fact that incomes were up a little in January, higher by 0.3% (per hour income was up 0.4%). And in true American-consumer fashion, spending was up by a little more, growing by 0.4% last month. It shows that consumers are still feeling relatively confident, even if they say they're not.

It wasn't all sunshine and roses last week, however. January's factory orders fell 0.7%, following December's 2.0% plunge.

Although there was plenty more data spewed out last week, much of it wasn't particularly important. It's all on the following grid.

Economic Calendar

The coming week won't be as busy, and even lass of that data will be worth worrying about. In fact, the only economic item of real consequence this week is Thursday's retail sales numbers for February. The pros say they should by up 0.2%, with or without cars. It'll be a nice turnaround from January's tepid sales.

The only other data of real interest in the lineup this week is Friday's producer price index information for February, and it's only interesting as a precursor for the following week's consumer price index data. As it stands right now, the annualized producer price inflation rate is 1.6%, and last month's data is roughly expected to jive with that. For reference, the annualized consumer inflation rata currently stands at 1.58%.

Stock Market Index Analysis

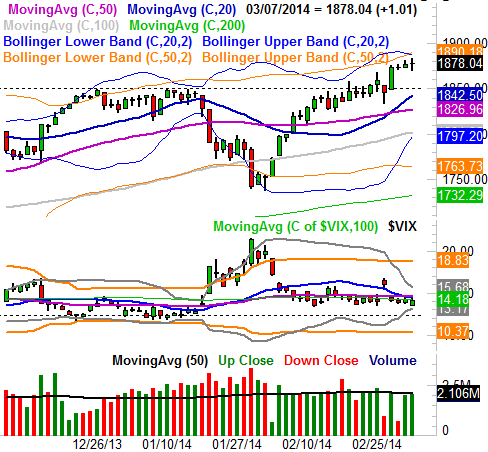

Last week, the S&P 500 (SPX) (SPY) gained 18.59 points (+1.0%), ending Friday's session at 1878.04. That's a record high close; the index also hit a record high of 1883.57 on Friday.

On the surface the data seems bullish, and it is. On the other hand, when you take a decently-closer look at the S&P 500's daily chart, it looks like the rally's running out of gas. Had it not been for Tuesday's 1.5% rebound, the index would have actually lost ground last week. It's also curious that we saw a doji-shaped candlestick bar on Friday, with an open and close right in the middle of a rather tall bar that was formed after a pretty solid runup. It's a sign that the bulls are running out of steam. It should be a small worry for the bulls…. though we reiterate, a "small" one at this point.

S&P 500 & VIX – Daily Chart

See the volume bars at the bottom of the chart? The two bearish days (Monday and Wednesday) with both low-volume days. The other three bullish days (Tuesday, Thursday, and Friday) were all high-volume days. Point being, there are still more buyers than sellers a this point.

That doesn't mean the market's equipped to make progress every single day from here forward, however. The good news is, the bulls have some room to let the S&P 500 slide back and cool off before breaking under any major support levels. The former ceiling at 1849 is now likely to be a floor, especially now that the 20-day moving average line (blue) is in the verge of reaching the same level. In fact, a small pullback to that level may actually be the best thing that could happen for the bulls right now, undoing any overbought-ness the market's experience right now.

The X-factor is the CBOE Volatility Index (VIX) (VXX). It's already oddly low, but it doesn't seem like it's got the ability or willingness to break above its key short-term moving average lines around 15.0. Until the VIX can poke above that convergence of moving averages and actually let the S&P 500 pull back a little, the market's upside is going to be limited… at least in terms of pace. The trouble is (once again), getting the VIX back up to much higher levels with the S&P 500 not breaking under the key floor at 1849.

Yes, it's something of a narrow path the bulls must walk if the rally is going to last any length of time, starting a modest – but only a modest – dip.

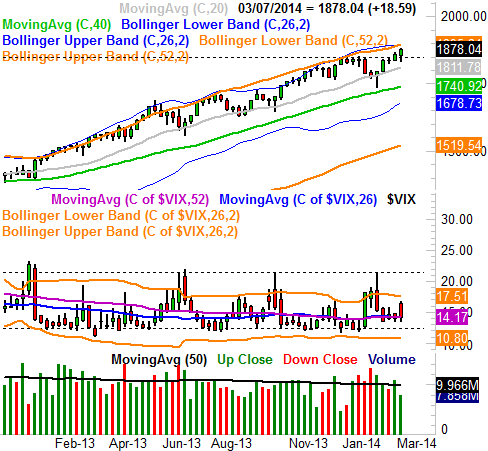

Does anything change when you zoom out to a weekly chart? Not really. It's here we can see that the bigger uptrend is still bullish, and that the S&P 500 has been finding support on a pretty regular basis since early 2013. The 100-day moving average line (gray), currently at 1812, is that floor… give or take.

S&P 500 & VIX – Weekly Chart

It's worth noting that on the weekly chart we can see how the VIX can pop higher without pushing the S&P 500 over the cliff to where it can't recover. Three times since mid-2013 have we seen the VIX reach a key ceiling at 21.40 without causing a complete breakdown for the market. All of those "resets" for the VIX pulled the S&P 500 just a bit under its 100-day moving average line (gray) currently at 1812, so there actually is a way for the index to break under the 1849 mark without going into meltdown mode. Ideally though, the VIX can move much higher without forcing the S&P 500 to suffer that much damage.

Whatever the case, the bigger trend remains bullish and we remain in a buy-on-the-dip environment.

Trade Well,

Price Headley

None.