How Fiat Money Made Beef More Expensive

In my article on the gold standard published in the Journal of Libertarian Studies back in May, I suggested that the destruction of the gold standard led to changing consumption patterns, specifically to a drop in the consumption of beef. The eminent economist George Selgin was kind enough to suggest that this was a novel argument, although in truth, in that essay I did no more than hint en passant at a possible connection between fiat money and changing consumption patterns, without explaining what the causal factors at work are. Therefore, I think the thesis bears restating and expanding upon.

Changing Food Consumption Patterns in the Twentieth Century

The change in meat consumption was a global phenomenon, but for present purposes, I will focus on the American case, although the same causal factors are at work, and probably to a greater extent, in the rest of the world. The US Department of Agriculture’s Economic Research Service (ERS) compiles and publishes copious data on food availability, that is, how much of various foods are available to the American consumer. Various kinds of meat are partial substitutes for each other, as are, of course, other foodstuffs; however, it seems a fair assumption to say that, in general, people would consider beef, pork, and poultry (the top three types of meat) the closest substitutes. Only in extreme cases would one consider, say, soya substitute for tasty beef.

The ERS dataset for meats covers the period 1909–2019 and measures availability in pounds per capita. In 1909, there were 51.1 pounds of beef, 41.2 pounds of pork, and 10.4 pounds of chicken available per capita, for a total of 102.7 pounds of all meats per capita. In 2019 the figures were, respectively, 55.4, 48.8, and 67.0 per capita, for a total of 171.2 pounds of all meats per capita. While meat consumption had gone up, the composition of the diet had changed drastically. If we add the fact that veal and delicious lamb, minor components in 1909 at 5 and 4.4 pounds per capita, respectively, had virtually disappeared from the diet in 2019, the change becomes even more noticeable.

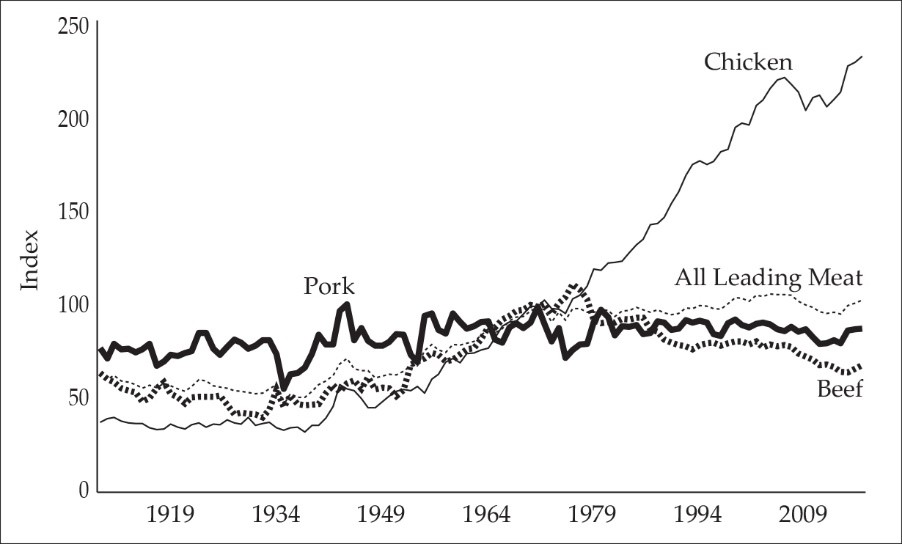

The following graph indexes the changing composition of meat availability over the century (1971=100). As we see, there is a steady and drastic rise in chicken availability from about the early 1950s, while the expansion of beef availability peaks in 1976 and then drops steadily back toward the 1909 level. While the availability of all meats expands until about 1970, it stagnates thereafter.

(Click on image to enlarge)

Source: Kristoffer Mousten Hansen, “The Populist Case for the Gold Standard,” Journal of Libertarian Studies 24, no. 2 (2020): figure 6. Data from ERS Food Availability (Per Capita) Data System.

If we look at changes in the relative prices of the various foodstuffs over the long run, a similar picture emerges. Beef prices have increased since the middle of the twentieth century, while other prices have fallen.

(Click on image to enlarge)

Source: Data from David S. Jacks, “From Boom to Bust: A Typology of Real Commodity Prices in the Long Run,” Cliometrica 13, no. 2 (2019): 202–20, Data on Real Commodity Prices, 1850–present online dataset.

Unfortunately, poultry prices are not listed in the dataset. However, we can approximate them by looking at grain prices, as this is a main input in the raising of chicken.

(Click on image to enlarge)

Source: Jacks, Data on Real Commodity Prices, 1850–present.

I have here chosen barley and corn prices, but it does not matter much, since the trend is similar for the prices of all grains. Prices have decreased since midcentury despite some fluctuations in the seventies and are now far below the level that prevailed for decades. Beef prices, on the contrary, have trended much higher and were in 2020 about double the level in 1900 or 1850. If we consider the relative price of beef, it is much, much higher, so we should not be surprised that meat consumption has shifted to cheaper substitutes: pork and especially chicken. It is clear that a fundamental change has happened in modern food production.

The Monetary Causes of Changing Food Production1

The price data presented above might itself suggest that this change originates in the monetary order. Until the second decade of the twentieth century, prices were, overall, pretty stable. There were fluctuations from each year to the next, but not the kind of long-term changes that set in afterward. This coincides with the era of sound money, when money was a commodity (silver or, from 1870 almost exclusively, gold) and had to be produced as any other commodity: if you wanted more money, you had to give something else in exchange for it. It did not matter if you chose to acquire more money by producing other goods and exchanging them or investing your own labor and capital in gold mines; the economic consequences were the same.

This changed, as is well known, with the destruction of the gold standard in 1914 and the introduction of increasingly inflationary monetary systems after the world wars. However, inflation cannot, in itself, explain the changing pattern of food production. Inflation, after all, leads to redistribution of wealth and short-term dislocations and malinvestments—but long term, it results in higher prices for all goods. Since what we have experienced is a much greater supply of and lower price for chicken especially relative to beef, simply positing inflation does not explain anything.

Another way of conceiving the change is as a trend of productivity increases and lower costs in the production of grains and chicken relative to beef. As simple inflation is a demand-side phenomenon—more money chasing fewer goods, in the Friedmaniac phrase—looking at the supply side might seem to exclude the possibility of monetary causes. However, as Ludwig von Mises clearly explained, in the modern fiat system, the creation of money is intimately connected with the extension of credit. While credit expansion was possible under the gold standard, the need for gold redemption put an inevitable brake on the process after a few years, ensuring that it was always kept within narrow bounds. In the monetary system set up after World War II, however, there are essentially no such brakes. Banks now have a much wider scope for credit expansion, as the central bank stands ready to supply them with reserves as needed and to bail them out when the inevitable, but now much delayed, bust arrives. Instead of intermediating credit, banks create the money they lend, and they can therefore consistently charge a rate of interest lower than the natural rate, as contrary to appearances, their profits accrue not from credit intermediation, but from money creation.

This necessarily leads to a change in investment patterns, as bank credit increasingly dominates. Some sources of capital, such as cash savings, are now made virtually impossible due to the inherently inflationary nature of the system, and equity financing is generally discouraged, as bank loans at low interest rates are so much more attractive. Not does only the source of capital change, but also the kind of investment: enterprises become more “capitalistic” as it were; they invest in capital goods and new production processes that increase the physical productivity of their plants. Present productivity is boosted at the cost of long-term plans that might have been more value productive.

This is true in agriculture as well and is evidenced by the huge increase in physical productivity in agriculture since the late 1940s. However, such productivity increases are simply not possible in the case of cattle and beef production. A cow needs a certain minimum acreage of land to live; she needs a grass-based diet, which in turn requires extensive pastures and hayfields and so on. While it is possible to supplement with other feeds, and while it is, of course, possible to increase the productivity of more extensive cultivation as well, such possibilities are dwarfed by the developments in the production of pork, chicken, and other commodities. An area of land which previously could be used to raise a herd of cattle or produce a quantity of grain can after ten or twenty years’ time be used to raise a herd of the same size—or two or three times the quantity of grain. The opportunity costs of raising cattle are thus constantly increasing.

Looking more narrowly at poultry and pork production, here we have also witnessed huge increases in productivity due to bank-fueled investment. New production methods and investment in modern plants have tamed the natural life cycles of piglets and chicks alike and brought them almost completely under human control, opening the way to mass production. So far, at least, this has proved impossible in the case of cattle rearing.2 Despite hyped stories about feedlots, the modern factory farm is real only when it comes to pork and poultry production. These enterprises and plants have a much wider scope for the investment of the kind that banks are willing to finance, and hence they will continue to expand and increase productivity relative to beef production.

Conclusion

Once we recognize the intimate connection between credit expansion and money production in the modern financial system, we can see how deeply fiat money and privileged banking distort the economic order. Banks earn seigniorage—the profit from money creation—by extending loans, and can therefore outcompete other sources of financing, be it people’s personal savings or independent lenders. As a result, credit is centralized in the system of credit-expanding banks and investment decisions are dictated by the short-term logic of the said system. Changing diets is just one consequence of the distortions engendered, albeit one that no one, pace Selgin, has investigated until now.

Since investment has flown into the production of grains, pork, and poultry, productivity in these fields has increased more than in beef production, and the supply of these foodstuffs has risen while their prices have fallen relative to the supply and price of beef. People’s food budgets are generally pretty fixed, meaning that even though incomes rise the extra income goes to the purchase of other consumer goods, not food, a generalization known as Engel’s law.3 Beef therefore increasingly becomes a luxury, something only regularly consumed by the well-to-do, which working-class and lower-middle-class people only enjoy on special occasions. Had the gold standard endured, this distortion of production patterns and diets might not have happened. We might then, perhaps, have had to do without KFC and Chick-fil-A, but then again, Chick-fil-A is only a palliative when a man is constrained to subsist principally on chicken, the broccoli of meats.

- 1 The following is based on research from my doctoral dissertation, “Monetary Systems and Industrial Organization: The Case of Agriculture,” to be defended in December.

- 2. Douglas W. Allen and Dean Lueck, The Nature of the Farm: Contracts, Risk, and Organization in Agriculture (Cambridge, MA: Massachusetts Institute of Technology Press, 2002).

- 3. Engel’s law is, in reality, a necessary consequence of the law of diminishing marginal utility, a point first suggested by the Italian economist Paolo Leon in 1967 and which I prove in my dissertation.

Disclaimer: Riki nema disclaimer.

Comments

No Thumbs up yet!

No Thumbs up yet!