Investing In Semiconductor Earnings Growth

The PC industry isn't dead yet.

Intel (INTC - Trend Report) recently posted strong second quarter results, driven in part by strong demand in its core server and PC markets.

Following the Q2 report, analysts revised their estimates significantly higher for both 2014 and 2015. This sent the stock to a Zacks Rank #1 (Strong Buy).

Intel is the world's largest supplier of microprocessors with over 75% of worldwide market share among traditional PCs and servers.

Second Quarter Results

Intel delivered strong second quarter results on July 15. Earnings per share came in at 55 cents, beating the Zacks Consensus Estimate of 52 cents. It was a 41% increase over the same quarter last year.

Net revenue grew 8% year-over-year to $13.831 billion, well ahead of the consensus of $13.622 billion. This was driven by solid demand in its core server and PC markets. Intel's Data Center (server) group saw top-line growth of 19% year-over-year, while its PC Client Group saw revenue growth of 6%.

Gross profit as a percentage of total revenue improved greatly. The gross margin rose from 58.3% to 64.5%. Meanwhile, marketing, general and administrative expenses declined 5% and fell from 16.9% to 14.9% of revenue.

These factors led to a whopping 41% surge in operating income as the operating margin expanded 21.2% to 27.8%.

Earnings Outlook

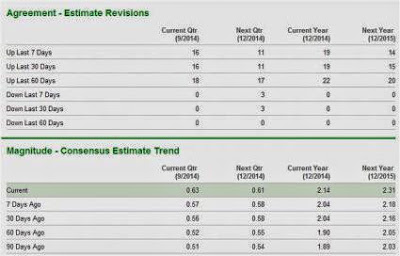

Following the strong Q2 results, analysts have unanimously raised their estimates for both 2014 and 2015. This has sent the stock to a Zacks Rank #1 (Strong Buy).

Part of the catalyst for the upward revisions was encouraging guidance from management, which stated in the Q2 report that it expects about 5% revenue growth in 2014. That is slightly higher than its previous guidance.

The Zacks Consensus Estimate for 2014 is now $2.14, up from $2.04 before the report. The 2015 consensus is now $2.31, up from $2.18 over the same period.

Intel still faces long-term challenges as it struggles to gain traction in the growing tablet and smartphone markets. But the near-term outlook looks bright for the stock as the PC industry appears to be stabilizing after two years of contraction.

Valuation

Shares of Intel soared after the Q2 report and have been on a tear this year, rising more than +32%. But the valuation picture still looks reasonable. Shares trade around 16x 12-month forward earnings and about 9x cash flow.

In addition, the company pays a dividend that yields a solid 2.7%.

The Bottom Line

Intel has a dominant position in the microprocessor industry for traditional PCs and servers. And thanks to recent strength in these end markets, along with solid cost controls from the company, earnings growth - and earnings estimates - are soaring for Intel.

Disclosure: None.