Morning Call For Aug. 20, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 unch) this morning are down -0.08% and European stocks are down -0.26% ahead of the release of the minutes of the Jul 29-30 FOMC meeting later today. The markets are also looking ahead to comments from Fed Chair Yellen and ECB President Draghi from the annual 2-day Fed conference that begins tomorrow in Jackson Hole, Wyoming. Asian stocks closed mixed: Japan +0.03%, Hong Kong +0.15%, China-0.36%, Taiwan +0.48%, Australia +0.19%, Singapore +0.22%, South Korea +0.06%, India -0.40%. Commodity prices are mixed. Sep crude oil (CLU14+1.29%) is up +1.53%. Sep gasoline (RBU14 +0.62%) is up +0.81%. Dec gold (GCZ14 +0.01%) is down -0.13%. Sep copper (HGU14 +0.62%) is up +0.57%. Agriculture and livestock prices are mostly lower. The dollar index (DXY00 +0.22%) is up +0.26% at an 11-1/4 month high on speculation today's minutes from the Jul 29-30 FOMC meeting will show policy makers are moving toward raising interest rates. EUR/USD (^EURUSD) is down-0.31% at an 11-1/4 month low on deflation concerns after German Jul producer prices unexpectedly declined. USD/JPY (^USDJPY) is up +0.39% at a 4-1/4 month high on speculation that the BOJ may cut its growth forecast for this fiscal year for a fourth time as exports fail to bolster the Japanese economy weakened by April's sales-tax increase. GBP/USD rebounded from a 4-1/4 month low after minutes of the Aug 6-7 BOE meeting showed two policy makers voted for an interest rate increase. Sep T-note prices (ZNU14 -0.09%) are down -1 tick.

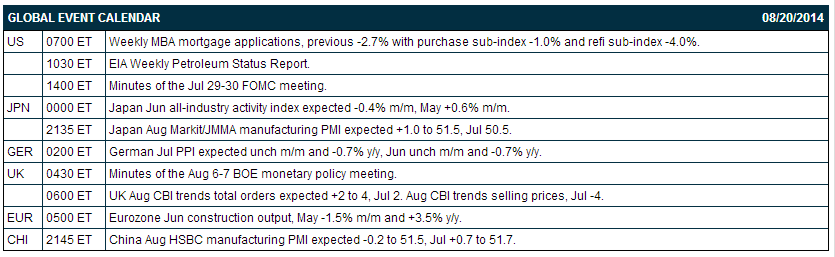

The Japan Jul trade balance unexpectedly widened to a -964.0 billion yen deficit from a revised -823.2 billion deficit in Jun, more than expectations for the deficit to narrow to -713.9 billion yen. Jul exports rose +3.9% y/y, slightly better than expectations of +3.8% y/y, while Jul imports unexpectedly rose +2.3% y/y, better than expectations of -1.5% y/y.

The Japan Jun all-industry activity index fell -0.4% m/m, right on expectations.

German Jul PPI fell -0.1% m/m and -0.8% y/y, a faster pace of decline than expectations of unch m/m and -0.7% y/y.

Eurozone Jun construction output fell -0.7% m/m and -2.3% y/y.

UK Aug CBI trends of manufacturing orders rose +9 to 11, stronger than expectations of +2 to 4. The Aug trends of selling prices fell to -1, a slower pace of decline than from -4 in Jul.

U.S. STOCK PREVIEW

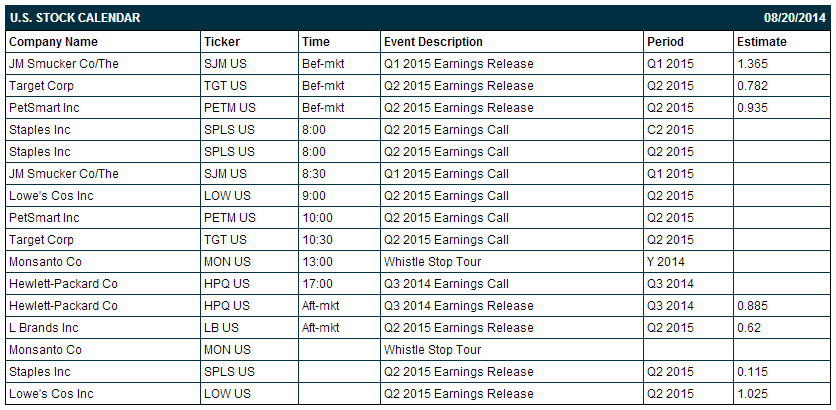

The FOMC today will release the minutes from its July 29-30 meeting. The markets will also be watching today’s weekly MBA report for an update on mortgage and housing market activity. There are seven S&P 500 companies that reports earnings today: JM Sucker (consensus $1.37), Target (0.78), PetSmart (0.94), Hewlett-Packard (0.885), L Brands (0.62), Staples (0.115) and Lowe's ($1.025). Equity conferences this week include: Enercom, Inc Oil & Gas Conference on Mon-Thu, and 8th Annual Forum on Transparency & Aggregate Spending on Tue-Wed.

OVERNIGHT U.S. STOCK MOVERS

JM Smucker (SJM +0.31%) reported Q1 EPS of $1.34, less than consensus of $1.37

Staples (SPLS +0.78%) reported Q2 EPS of 12 cents, right on expectations.

Lowe's (LOW +2.12%) reported Q2 EPS of $1.04, higher than consensus of $1.03.

UBS maintains its 'Buy' rating on Home Depot (HD +5.55%) and raised its price target on the stock to $98 from $91.

Hain Celestial (HAIN -2.00%) reported Q4 adjusted EPS of 90 cents, higher than consensus of 89 cents.

Panera Bread (PNRA +1.89%) was upgraded to 'Overweight' from 'Equal Weight' at Barclays.

BHP Billiton (BHP -3.75%) was downgraded to 'Underperform' from 'Neutral' at Credit Suisse.

PetSmart (PETM +1.84%) gained over 1% in after-hours trading after it reported Q2 EPS of 98 cents, better than consensus of 94 cents.

Hertz (HTZ +1.28%) slumped over 12% in after hours trading after it withdraw guidance for fiscal 2014. The stock was then downgraded to 'Neutral' from 'Overweight' at JPMorgan and downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Oz Management reduced its stake in Rockwood (ROC -0.20%) to 3.5% from 5.95%.

RA Capital reported a 6.2% passive stake in Vical (VICL unch) .

La-Z-Boy (LZB +2.79%) slipped over 3% in after-hours trading after it reported Q1 EPS of 20 cents, below consensus of 21 cents.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 unch) this morning are down -1.50 points (-0.08%). The S&P 500 index on Tuesday posted a 3-week high and settled higher: S&P 500 +0.50%, Dow Jones +0.48%, Nasdaq +0.49%. Supportive factors for stocks included (1) the +15.7% jump in U.S. Jul housing starts to 1.093 million, well above expectations of +8.1% to 965,000 and the most in 8 months, (2) the +8.1% gain in Jul building permits, a proxy for future construction, to 1.052 million, stronger than expectations of +2.8% to 1.000 million, and (3) tame inflation data after Jul CPI ex-food & energy rose +0.1% m/m and +1.9% y/y, slightly less than expectations of +0.2% m/m and +1.9% y/y.

Sep 10-year T-notes (ZNU14 -0.09%) this morning are down -1 tick. Sep 10-year T-note futures prices on Tuesday closed lower. Stronger-than-expected U.S. Jul housing starts boosted the S&P 500 to a 3-week high and undercut T-notes, while benign U.S. inflation data for July kept T-note losses to a minimum. Closes: TYU4 -4.5, FVU4 -2.0.

The dollar index (DXY00 +0.22%) this morning is up +0.212 (+0.26%) at a new 11-1/4 month high. EUR/USD (^EURUSD) is down -0.0041 (-0.31%) at an 11-1/4 month low and USD/JPY (^USDJPY) is up +0.40 (+0.39%) at a 4-1/4 month high. The dollar index on Tuesday soared to an 11-month high and closed higher. Bullish factors included (1) signs the U.S. economy is gaining traction after Jul housing starts rose to an 8-month high, and (2) weakness in EUR/USD which fell to a 9-1/4 month low on weakened interest rate differentials for the euro versus the dollar on expectations for the Fed to tighten monetary policy before the ECB. Closes: Dollar index +0.307 (+0.38%), EUR/USD -0.00433 (-0.32%), USD/JPY +0.345 (+0.34%).

Sep WTI crude oil (CLU14 +1.29%) this morning is up +$1.45 (+1.53%) and Sep gasoline (RBU14 +0.62%) is up +0.0217 (+0.81%). Sep crude and gasoline prices on Tuesday settled mixed with Sep crude falling to a 7-month low: CLU4 -1.93 (-2.00%), RBU4 +0.0503 (+1.89%). Bearish factors for crude prices included (1) the surge in the dollar index to an 11-month high, and (2) speculation that Wednesday's EIA data will show crude supplies at Cushing, OK, the delivery point for WTI futures, rose as the shutdown of the Coffeyville, Kansas refinery reduced demand for crude from Cushing. Gasoline prices gained on signs of economic strength after U.S. Jul housing starts rose to an 8-month high.

Disclosure: None