Morning Call For Aug. 27, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 +0.06%) this morning are up +0.04% on increased optimism in the U.S. economic outlook, while European stocks are down -0.16% after a gauge of German consumer confidence fell more than expected. Stocks received a boost on comments from Russian President Putin who met his Ukrainian counterpart in Belarus to discuss an end to the ongoing conflict and said that "Russia, for its part, will do everything for this peace process." European bond markets continue to rally as 10-year yields from Germany, Italy, Spain and France all fell to record lows on speculation the ECB will expand stimulus. Asian stocks closed mostly higher: Japan +0.09%, Hong Kong -0.62%, China +0.15%, Taiwan +0.98%, Australia +0.24%, Singapore +0.55%, South Korea +0.28%, India +0.44%. Commodity prices are mostly higher. Oct crude oil (CLV14 +0.29%) is up +0.28%. Oct gasoline (RBV14 +0.33%) is up +0.23%. Dec gold (GCZ14 +0.05%) is up +0.12%. Sep copper (HGU14 -0.06%) is up +0.06%. Agriculture and livestock prices are mixed. The dollar index (DXY00 -0.14%) is down -0.13% as it retreats from an 11-1/2 month high. EUR/USD (^EURUSD) is up +0.11% as it recovers from an 11-1/2 month low after comments from German Finance Minister Schaeuble fueled short covering when he said that comments made by ECB President Draghi that advocate support for Eurozone fiscal policy were "over-interpreted." USD/JPY (^USDJPY) is down -0.12%. Sep T-note prices (ZNU14 +0.09%) are up +4.5 ticks on carry-over support from a rally in European government bond markets.

German Finance Minister Schaeuble said in an interview in the Passauer Neue Presse that comments made in Jackson Hole, Wyoming by ECB President Draghi were "over-interpreted" after he said that fiscal policy could play a greater role in promoting growth.

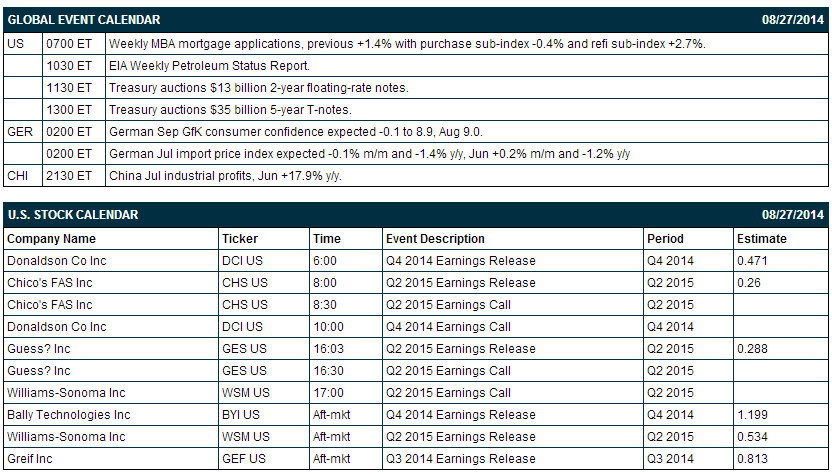

The German Jul import price index fell -0.4% m/m and -1.7% y/y, a faster pace of decline than expectations of -0.1% m/m and -1.4% y/y.

The German Sep GfK consumer confidence fell -0.3 to 8.6, a larger decline than expectations of -0.1 to 8.9.

U.S. STOCK PREVIEW

The Treasury today will sell $35 billion of 5-year T-notes and $13 billion of 2-year floating-rate notes. The markets will be watching today’s MBA mortgage apps report for an update on mortgage activity. The MBA index last week rose by +1.4% with the purchase sub-index down by -0.4% and refinancing sub-index up by +2.7%.

There are 9 of the Russell 1000 companies that reports earnings today: Donaldson (consensus $0.47), Tiffany (0.85), Brown-Forman (0.72), Chico's FAS (0.26), Workday (-0.14), Bally Technologies (1.20), Williams-Sonoma (0.53), Greif (0.81), Seadrill (0.74). Equity conferences this week include: ONS 2014 Conference on Mon-Thu, Latin Markets 3rd Annual Peru Capital Projects & Infrastructure Summit on Wed, Simmons European Energy Conference on Wed, Jefferies Semiconductors, Hardware & Communications Infrastructure Summit on Wed, and MIT Sloan Latin America-China Conference on Fri.

OVERNIGHT U.S. STOCK MOVERS

Tiffany & Co. (TIF +0.54%) reported Q2 EPS of 96 cents, better than consensus of 85 cents.

Brown Shoe (BWS +0.51%) reported Q2 EPS of 41 cents, higher than consensus of 35 cents.

Eli Lilly (LLY +0.13%) was initiated with a 'Buy' at Deutsche Bank with a price target of $71 and Pfizer (PFE +1.04%) was also initiated with a 'Buy' at Deutsche Bank with a price target of $34.

Waste Management (WM +0.17%) was upgraded to 'Buy' from 'Hold' at Stifel.

Facebook (FB +1.25%) was downgraded to 'Neutral' from 'Buy' at Janney Capital.

Donaldson (DCI -0.15%) reported Q4 EPS of 50 cents, higher than consensus of 47 cents.

Rent-A-Center (RCII +0.95%) was upgraded to 'Buy' from 'Hold' at Canaccord.

Bristol-Myers (BMY +0.08%) announced that the European Commission has approved Daklinza for use in combination with other medicinal products across genotypes 1, 2, 3 and 4 for the treatment of chronic hepatitis C virus infection in adults.

Smith & Wesson (SWHC -0.08%) slumped over 10% in after-hours trading after it said its sees Q2 EPS of 4 cents-8 cents, well below consensus of 28 cents, and lowered guidance on fiscal 2015 EPS to 89 cents-94 cents, much weaker than consensus of $1.36.

FJ Capital reported a 5.87% passive stake in Sun Bancorp (SNBC +0.52%) .

Dycom (DY +1.20%) reported Q4 EPS of 48 cents, better than consensus of 47 cents.

Bob Evans (BOBE -2.73%) reported Q1 adjusted EPS of 10 cents, right on consensus, although Q1 revenue of $326.3 million was slightly below consensus of $328.61 million.

Analog Devices (ADI +0.54%) reported Q3 EPS of 63 cents, right on consensus, although Q3 revenue of $728 million was higher than consensus of $716.69 million.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 +0.06%) this morning are up +0.75 of a point (+0.04%). The S&P 500 index and the Dow on Tuesday rallied to new all-time highs and closed higher: S&P 500 +0.11%, Dow Jones +0.17%, Nasdaq +0.10%. Bullish factors included (1) the +22.6% surge in Jul durable goods orders, well above expectations of +8.0% and the most since the data series began in 1992, and (2) the unexpected +2.1 increase in U.S. Aug consumer confidence to 92.4, better than expectations of -1.9 to 89.0 and the highest in 6-3/4 years. Gains in stocks were limited after the Jun S&P/CaseShiller composite-20 home price index fell -0.20% m/m, weaker than expectations of unch m/m.

Sep 10-year T-notes (ZNU14 +0.09%) this morning are up +4.5 ticks. Sep 10-year T-note futures prices Tuesday closed slightly higher. Bullish factors included (1) carry-over support from a rally in European government bonds after 10-year bond yields in Italy, Finland and Spain all dropped to record lows, and (2) the unexpected decline in U.S. Jul durable goods orders ex-transportation. Bearish factors included (1) reduced safe-haven demand after the S&P 500 rallied to a new record high, and (2) the unexpected increase in Aug consumer confidence to a 6-3/4 year high. Closes: TYU4 +2.5, FVU4 +3.00.

The dollar index (DXY00 -0.14%) this morning is down -0.108 (-0.13%). EUR/USD (^EURUSD) is up +0.0015 (+0.11%) and USD/JPY (^USDJPY) is down -0.12 (-0.12%). The dollar index on Tuesday closed higher. Bullish factors included (1) the unexpected increase in U.S. Aug consumer confidence to a 6-3/4 year high, and (2) the slide in EUR/USD to an 11-1/2 month low on divergent central bank policies as the Fed is expected to continue to taper stimulus while the ECB looks to expand monetary stimulus. Closes: Dollar index +0.101 (+0.12%), EUR/USD -0.00249 (-0.19%), USD/JPY +0.006 (+0.01%).

Oct WTI crude oil (CLV14 +0.29%) this morning is up +26 cents (+0.28%) and Oct gasoline (RBV14 +0.33%) is up +0.0061 (+0.23%). Oct crude and gasoline prices on Tuesday closed higher with Oct gasoline at a 1-week high: CLV4 +0.51 (+0.55%), RBV4 +0.0047 (+0.18%). Bullish factors included (1) increased optimism in the U.S. economic outlook after the S&P 500 posted a new record high, and (2) expectations that Wednesday’s weekly EIA inventory report will show crude stockpiles fell -2.5 million bbl and gasoline supplies fell -1.6 million bbl.

Disclosure: None