Morning Call For Aug. 4, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 +0.36%) this morning are up +0.35% and European stocks are up +0.72% as Portuguese government bonds rallied and corporate credit risk in Europe fell for the first time in 5 days after the Bank of Portugal said Banco Espirito Santo SA will receive a 4.9 billion euro ($6.6 billion) bailout. Asian stocks closed mixed: Japan -0.31%, Hong Kong +0.28%, China +1.98%, Taiwan +0.69%, Australia -0.28%, Singapore-0.78%, South Korea +0.41%, India +0.95%. China's Shanghai Stock Index rallied to a 7-3/4 month high as Chinese brokerage companies rose on a report that the government plans to relax some risk-management requirements on securities companies that could free up capital for expansion. Chinese stocks rallied despite a drop in the China Jul non-manufacturing PMI to a 6-month low. Commodity prices are mixed. Sep crude oil (CLU14+0.18%) is up +0.22%. Sep gasoline (RBU14 -0.30%) is down -0.12%. Dec gold (GCZ14 -0.21%) is down -0.17%. Sep copper (HGU14 +0.25%) is up +0.06%. Agriculture prices are higher. The dollar index (DXY00 +0.09%) is up +0.08%. EUR/USD (^EURUSD) is down -0.04% after Eurozone Aug Sentix investor confidence fell more than expected to a 1-year low. USD/JPY (^USDJPY) is up +0.01%. Sep T-note prices (ZNU14 +0.05%) are up +3 ticks.

The Bank of Portugal (BOP) took over Banco Espirito Santo SA in a 4.9 billion euro bailout. The BOP said that it will take control of Banco Espirito Santo's assets and deposit-taking operations by transferring them to a new company, Novo Banco, into which it will inject funds from its Resolution Fund. The fund will finance the rescue with a Treasury loan to be repaid by Novo Banco's eventual sale.

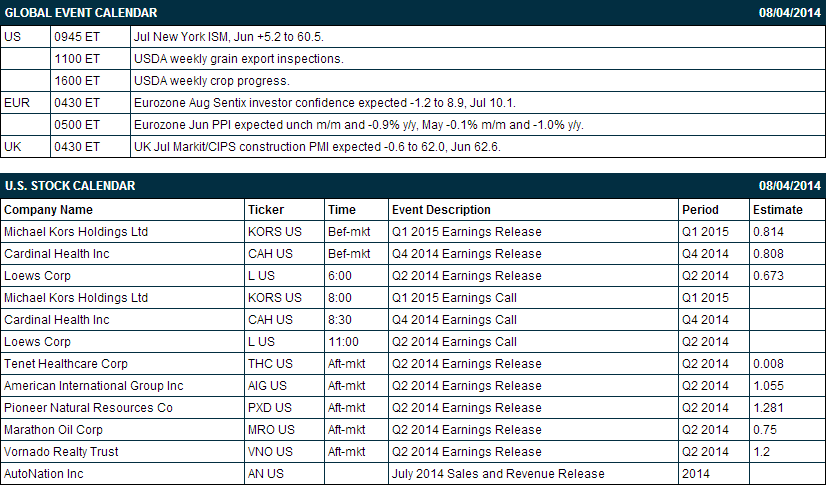

Eurozone Aug Sentix investor confidence fell -7.4 to 2.7, a bigger decline than expectations of -1.1 to 9.0 and the lowest in a year.

Eurozone Jun PPI rose +0.1% m/m and fell -0.8% y/y, stronger than expectations of unch m/m and -1.0% y/y.

The UK Jul Markit/CIPS construction PMI fell -0.2 to 62.4, a smaller decline than expectations of -0.6 to 62.0.

The China Jul non-manufacturing PMI fell -0.8 to 54.2, the slowest pace of expansion in 6 months.

U.S. STOCK PREVIEW

This week’s U.S. economic schedule is light, but the market will have carry-over concerns from last week including the Argentina default, banking problems in Portugal, Russian sanctions, and when the Fed might raise interest rates. This will be another fairly busy Q2 earnings week. The Treasury on Wednesday will announce next week’s sale of 3, 10 and 30-year securities.

There are 8 of the S&P 500 companies that report earnings today with notable reports including: Marathon Oil (consensus $0.75), AIG (1.06), Tenet Healthcare (0.01), Pioneer Natural Resources (1.28). Equity conferences this week include: Needham Interconnect Conference on Tue, Piper Jaffray Global Agriculture & Animal Health Investor Day on Tue, AESP Conference - Evaluators & Implementers: Merging on the Energy Efficiency on Tue, CFA Society of Minnesota InvestMNt Conference on Wed, Black Hat USA 2014 on Wed-Thu, Needham Advanced Industrial Technologies Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Loews (L +0.28%) reported Q2 EPS of 79 cents, higher than consensus of 67 cents.

Michael Kors Holdings (KORS +0.43%) reported Q1 EPS of 91 cents, well above consensus of 81 cents.

Cardinal Health (CAH +1.00%) reported Q4 EPS of 83 cents, better than consensus of 81 cents.

Alere (ALR -0.12%) reported Q2 adjusted EPS of 42 cents, well below consensus of 58 cents.

Henry Schein (HSIC +0.98%) reported Q2 EPS $1.35, better than consensus of $1.33.

T-Mobile (TMUS +1.46%) was upgraded to 'Overweight' from 'Equal-Weight' at Evercore.

Berkshire raises its passive stake in VeriSign (VRSN -1.57%) to to 10.4% from 8.0%.

Transocean (RIG +0.25%) and Diamond Offshore (DO +1.13%) were both downgraded to 'Sell' from 'Hold' at Deutsche Bank.

U.S. Steel (X -0.15%) was upgraded to 'Buy' from 'Hold' at Deutsche Bank.

Noble Corp. (NE -0.92%) and Ensco (ESV +0.55%) were both downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Alcatel-Lucent (ALU -1.75%) was upgraded to 'Overweight' from 'Equal Weight' at Morgan Stanley.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 +0.36%) this morning are up +6.75 points (+0.35%). The S&P 500 index on Friday tumbled to a 2-month low and closed lower: S&P 500 -0.29%, Dow Jones -0.42%, Nasdaq -0.33%. Bearish factors included (1) the +209,000 increase in July non-farm payrolls, weaker than expectations of +230,000,, (2) the unexpected +0.1 increase in the July unemployment rate to 6.2%, higher than expectations of unch at 6.1%, and (3) global banking concerns after Argentina failed to pay interest on its bonds is a credit event that will trigger settlement of $1 billion of default insurance and after Portugal’s securities regulator ordered Banco Espirito Santo to raise more capital.

Sep 10-year T-notes (ZNU14 +0.05%) this morning are up +3 ticks. Sep 10-year T-note futures prices on Friday closed higher. Bullish factors included (1) the smaller-than-expected increase in July non-farm payrolls and the unexpected uptick in the Jul unemployment rate, and (2) reduced wage inflation concerns after July avg hourly earnings were unch m/m, less than expectations of +0.2% m/m. Closes: TYU4 +20.50, FVU4 +15.00.

The dollar index (DXY00 +0.09%) this morning is up +0.065 (+0.08%). EUR/USD (^EURUSD) is down -0.0006 (-0.04%) and USD/JPY (^USDJPY) is up +0.01 (+0.01%). The dollar index on Friday closed lower after U.S. July non-farm payrolls rose less than expected, which curbed speculation the Fed would move up its pace of expected interest rate hikes next year. Closes: Dollar index -0.154 (-0.19%), EUR/USD +0.00394 (+0.30%), USD/JPY -0.200(-0.19%).

Sep WTI crude oil (CLU14 +0.18%) this morning is up +22 cents (+0.22%) and Sep gasoline (RBU14 -0.30%) is down -0.0032 (-0.12%). Sep crude and gasoline prices on Friday closed lower with Sep crude at a 6-month low and Sep gasoline at a 4-month low: CLU4 -0.29 (-0.30%), RBU4 -0.0575(-2.06%). Bearish factors included (1) demand concerns after the CEO of the CVR Refinery in Coffeyville, Kansas that uses crude from Cushing, OK said that the refinery may be closed for four weeks because of damage from a fire, which would curb demand and lead to increased stockpiles at Cushing and (2) gasoline demand concerns after EIA gasoline inventories rose to a 4-month high last Wed despite summer being typically a strong time of year for gasoline demand.

Disclosure: None