Morning Call For Oct. 10, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 -0.38%) this morning are down another -0.47% as concerns continue about slowing world economic growth. The EuroStoxx 50 Index this morning is down sharply by -1.42%. Asian stocks today closed lower across the board: Japan -1.15%, Hong Kong -1.90%, China CSI 300 index -0.61%, Australia -2.05%, Singapore -1.09%, South Korea -1.33%, India -1.20%, Turkey -1.24%. Dec 10-year T-note prices (ZNZ14+0.17%) this morning are up 7.5 ticks. The dollar index (DXY00 +0.29%) is up +0.16% today on safe-haven demand, while EUR/USD (^EURUSD) is down-0.16% and USD/JPY (^USDJPY) is down -0.15%.

Commodity prices are down another -0.30% today on expectations for weaker global demand. Nov WTI crude oil (CLX14 -1.12%) is sharply lower by-1.34% and Nov Brent crude is down -0.79%. Nov gasoline (RBX14 -1.27%) is down -1.38%. Dec gold (GCZ14 -0.15%) is down -0.24%, Dec silver (SIZ14-0.62%) is down -0.79%, and Dec copper (HGZ14 -0.99%) is down -1.07%. Grain and lean hog prices are lower while cattle is unchanged. Softs are mixed...

Oil prices are sharply lower again today as concern continues about a glut of oil and OPEC's apparent unwillingness as yet to cut production. Iran yesterday matched Saudi Arabia's discounts to customers in the crude oil market, indicating a price war among OPEC members. Kuwait and Iraq will release their selling prices next week.

The VIX index, which measures expected S&P 500 implied volatility, rose to 18.8% yesterday from as low as 12% in mid-September due to this week's sharp sell-off in stocks.

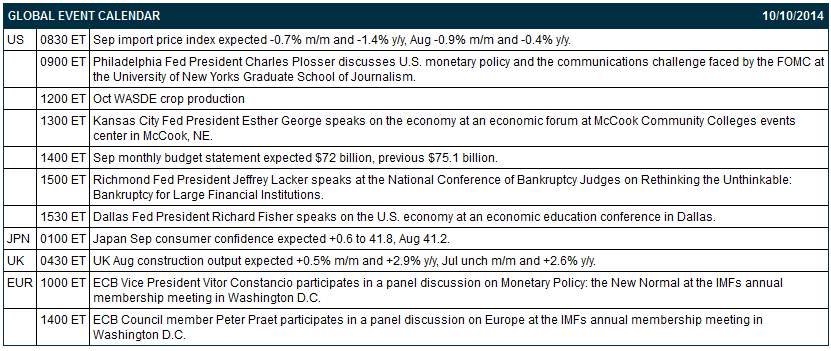

Today is a big day for Fedspeak with comments from Plosser, George, Fisher and Lacker.

South Korea today returned fire to what appeared to be heavy machine gun fire from North Korea across the border, the second time the two countries have exchanged fire this week. This comes as North Korean leader Kim Jong Un did not show up for today's key 69th anniversary of the founding of the ruling Workers' party. Kim has not been seen in public since Sep 3, sparking a variety of rumors about whether he is ill.

Japan's Sep consumer confidence index fell by -1.3 points to 39.9 from 41.2 in Aug, which was weaker than market expectations for a +0.6 point increase to 41.8.

The UK Aug visible trade deficit narrowed to -9.099 billion stlg from a revised -10.414 billion stlg in July and was narrower than market expectations of-9.60 billion stlg.

UK Aug construction output fell by -3.9% m/m and -0.3% y/y, which was weaker than market expectations of +0.5% m/m and +2.9% y/y.

U.S. STOCK PREVIEW

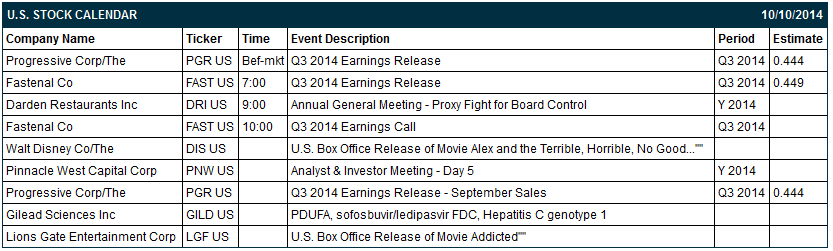

The market is expecting today’s Sep import price index to fall -0.7% m/m, adding to the sharp -0.9% m/m decline seen in August. The markets are expecting today’s Sep monthly budget statement to show a surplus of $72 billion, just below last year’s surplus $75.1 billion. There are two of the Russell 1000 companies that report earnings today: Progressive Corp (consensus $0.44), Fastenal (0.45). Equity conferences during the remainder of this week include: 2014 IIF Annual Membership Meeting on Fri.

Dec E-mini S&Ps this morning are down -9.00 points (-0.47%) on continued concern about weak global economic growth and on sharp sell-offs in overseas stock markets overnight. The S&P 500 index on Thursday closed sharply lower: S&P 500 -2.07%, Dow Jones -1.97%, Nasdaq -1.78%. Negative factors included (1) global economic concerns after German Aug exports fell -5.8% m/m, a larger decline than expectations of -4.0% m/m and the biggest monthly drop in 5-1/2 years, and (2) a slide in energy producers after crude oil prices tumbled to a 17-3/4 month low. On the positive side, weekly U.S. jobless claims unexpectedly fell -1,000 to 287,000, better than expectations of +8,000 to 295,000.

OVERNIGHT U.S. STOCK MOVERS

- Tesla (TSLA -0.88%) announced the all-wheel-drive version of its Model S with dual motors that can propel the car to 60 mph in 3.2 seconds.

- Fastenal (FAST -2.44%) reported July sales growth at +14.7% and Aug sales growth up +15%. FAST reported in-line fiscal Q3 EPS of 45 cents.

- Apple (AAPL +0.22%) will have only 3 days to review and block information in the GT Technology (GTAT +17.27%) bankruptcy case.

- Citigroup removed Liberty Interactive (QVCA -1.90%) from its Focus List but added adding HSN, Inc (HSNI -1.62%).

- PointState Capital reported a 6.0% passive stake in L-3 Communications (LLL -3.52%) .

- Highland Capital Management reported a 9.9% passive stake in Loral Space (LORL -3.32%) .

- Juniper (JNPR -1.23%) slipped 5% in after-hours trading after it lowered guidance on Q3 adjusted EPS to 34 cents-36 cents, below consensus of 38 cents, and lowered its Q3 revenue outlook to $1.11 billion-$1.12 billion, less than consensus of $1.18 billion.

- Family Dollar (FDO +0.05%) reported Q4 adjusted EPS of 73 cents, below consensus of 77 cents.

- Microchip (MCHP -1.43%) lowered Q2 revenue guidance to $546.2 million from $560.0 million-$575.9 million, below consensus of $567.91 million.

- Eminence Capital reported a 5.4% passive stake in TIBCO (TIBX -0.13%) .

MARKET COMMENTS

Dec 10-year T-notes this morning are up +7.5 ticks on safe-haven demand from today's continued sell-off in global stocks. Dec 10-year T-note futures prices on Thursday posted a contract high and closed higher. Bullish factors for T-notes included (1) carry-over strength from a rally in German bunds to a record high on Eurozone economic concerns after German Aug exports fell by the most in 5-1/2 years, and (2) increased safe-haven demand for T-notes after stocks fell sharply. Closes: TYZ4 +2.00, FVZ4 +0.50.

The dollar index this morning is up +0.14 points (+0.16%) on safe-haven demand. Meanwhile, EUR/USD is down -0.0020 (-0.16%) and USD/JPY is down-0.16 (-0.15%). The dollar index on Thursday recovered from a 2-week low and closed higher. Bullish factors included (1) signs of strength in the U.S. economy after weekly jobless claims unexpectedly declined, and (2) weakness in EUR/USD after German Aug exports fell by the most in 5-1/2 years and speculation the ECB may expand stimulus after ECB President Draghi said that the ECB must lift inflation from an “excessively low” level. Closes: Dollar index +0.225 (+0.26%), EUR/USD -0.00432 (-0.34%), USD/JPY -0.241 (-0.22%).

Nov WTI crude oil this morning is sharply lower by -1.15 (-1.34%) and Nov gasoline is down -0.0313 (-1.38%) as concern continues about weak global demand and an OPEC price war. Nov crude and Nov gasoline prices on Thursday closed lower with Nov crude at a 17-3/4 month low and Nov gasoline at a 3-3/4 year low: CLX4 -1.54 (-1.76%), RBXX4 -0.0435 (-1.88%). Bearish factors included (1) the rebound in the dollar as the dollar index recovered from a 2-week low and closed higher, and (2) global economic concerns after German Aug exports fell -5.8% m/m, the biggest drop in 5-1/2 years.

Disclosure: None