Morning Call For Oct. 27, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 -0.22%) this morning are down -0.20% and European stocks are down -0.55%. U.S. and European stocks had initially rallied up to 2-week highs in early trade Monday after the ECB said that most European banks passed stress tests, but stocks erased their gains and headed lower after German business confidence slid for a sixth month to the lowest in 1-3/4 years. Asian stocks closed mixed: Japan +0.63%, Hong Kong-0.68%, China -0.91%, Taiwan -0.21%, Australia +0.86%, Singapore +0.11%, South Korea +0.40%, India -0.37%. Japan's Nikkei Stock Index climbed to a 1-1/2 month high on optimism over U.S. stock earnings and after the ECB gave most European banks a clean bill of health following stress tests. Chinese stocks tumbled as the Shanghai Stock Index fell to a 1-3/4 month low after a Hong Kong bourse operator said that he had no idea when authorities will give the green light for cross-border trading between the two exchanges. Chinese stocks had rallied sharply in anticipation that price discounts versus Hong Kong stocks would narrow with the start of cross-border trading. Commodity prices are mostly lower. Dec crude oil (CLZ14 -0.52%) is down -0.53%. Dec gasoline (RBZ14 -0.48%) is down -0.87%. Dec gold (GCZ14 -0.08%) is down -0.10%. Dec copper (HGZ14 +0.31%) is up +0.07%. Agriculture prices are lower as dry, warm weather in the Midwest over the weekend sped up the pace of the U.S. harvest. The dollar index (DXY00 -0.07%) is down -0.08%. EUR/USD (^EURUSD) is up +0.01%. USD/JPY (^USDJPY) is down -0.26%. Dec T-note prices (ZNZ14 +0.02%) are down -0.5 of a tick.

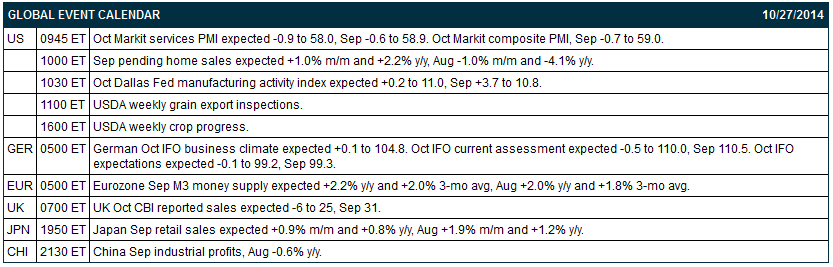

The German Oct IFO business climate fell -1.5 to 103.2, a larger decline than expectations of -0.2 to 104.5 and the lowest in 1-3/4 years. The Oct IFO current assessment fell -2.0 to 108.4, more than expectations of -0.5 to 110.0 and the lowest in 1-1/2 years. Oct IFO expectations dropped -1.0 to 98.3, a bigger decline than expectations of -0.1 to 99.2 and the lowest in 1-3/4 years.

Eurozone Sep M3 money supply rose +2.5% y/y and +2.1% 3-month average, more than expectations of +2.2% y/y and +2.0% 3-month average with the 2.5% y/y gain the largest annual increase in 16 months.

Data from the ECB showed that European bank lending to companies and households in Sep fell -1.2% y/y. Although it was an improvement from the-1.5% y/y fall in Aug, it was the 29th consecutive month that bank lending has shrunk.

Japan Sep PPI services rose +3.5% y/y, right on expectations and matched the largest increase in 23 years.

U.S. STOCK PREVIEW

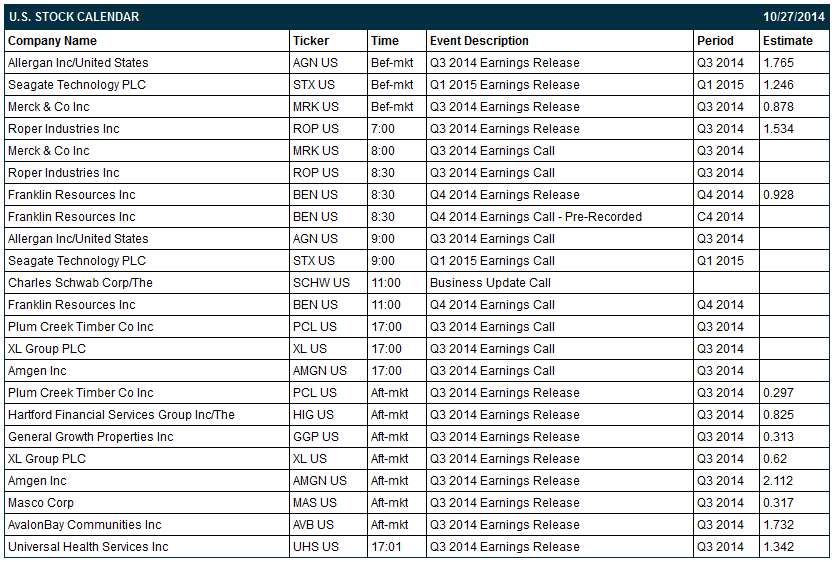

Today’s Sep pending home sales report is expected to show an increase of +1.0% m/m. There are 13 of the S&P 500 companies that report earnings today with notable reports including: Amgen (consensus $2.11), Seagate (1.25), Merck (0.88), General Growth (0.31), AvalonBay Communities (1.73). Equity conferences this week include: RMA Annual Risk Management Conference 2014 on Mon-Tue, and GTEC (Government Technology Exhibition & Conference) 2014 on Tue-Thu.

OVERNIGHT U.S. STOCK MOVERS

Allergan (AGN +0.46%) reported Q3 EPS of $1.72, below consensus of $1.77.

Merck & Co. (MRK +1.73%) reported Q3 EPS of 72 cents, weaker than consensus of 88 cents.

Roper Industries (ROP +0.43%) reported Q3 EPS of $1.55, better than consensus of $1.53.

Precision Drilling (PDS -1.99%) reported Q3 EPS of 18 cents, higher than consensus of 17 cents.

Armstrong World (AWI -0.14%) reported Q3 adjusted EPS of 83 cents, stronger than consensus of 78 cents.

Business Insider reports that Wal-Mart and Best Buy have joined Rite Aid and CVS Health in rejecting Apple's (AAPL +0.37%) mobile payments system Apple Pay.

Rackspace (RAX +0.98%) was upgraded to 'Buy' from 'Neutral' at BofA/Merrill Lynch.

Ventas (VTR -1.28%) was downgraded to 'Neutral' from 'Buy' at UBS.

Halliburton (HAL -0.13%) was downgraded to 'Buy' from 'Conviction Buy' at Goldman Sachs.

Anadarko (APC -1.29%) and EP Energy (EPE +1.64%) were both downgraded to 'Neutral' from 'Buy' at Goldman Sachs.

Precision Castparts (PCP -0.26%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Acuity Brands (AYI +0.76%) was upgraded to 'Conviction Buy' from 'Buy' at Goldman Sachs.

Alcoa (AA +1.91%) was upgraded to 'Buy' from 'Hold' at Deutsche Bank.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 -0.22%) this morning are down -4.00 points (-0.20%). The S&P 500 index on Friday rallied to a 2-week high and closed higher: S&P 500 +0.71%, Dow Jones +0.76%, Nasdaq +0.74%. Bullish factors included (1) strong Q3 stock earnings results with 70% of reporting S&P 500 companies beating estimates, and (2) an unexpected +0.2% increase in Sep new home sales to a 6-year high of 467,000 after Aug was revised lower to 466,000 from 504,000. Gains in stocks were limited on concern that the spread of the Ebola virus may slow the global economy after the first case of the virus was reported in New York City.

Dec 10-year T-notes (ZNZ14 +0.02%) this morning are down -0.5 of a tick. Dec 10-year T-note futures prices on Friday closed slightly higher on concern the spread of the Ebola virus will slow the economy and bolster the case for the Fed to delay raising interest rates. Closes: TYZ4 +0.50, FVZ4 +0.75. T-note prices fell back from their best levels after stocks rallied and after Sep new home sales climbed to a 6-year high.

The dollar index (DXY00 -0.07%) this morning is down -0.069 (-0.08%). EUR/USD (^EURUSD) is up +0.0001 (+0.01%). USD/JPY (^USDJPY) is down-0.28 (-0.26%). The dollar index on Friday closed lower. Closes: Dollar index -0.111 (-0.13%), EUR/USD +0.00232 (+0.18%), USD/JPY -0.125 (-0.12%). Bearish factors included (1) strength in EUR/USD after German Nov GfK consumer confidence unexpectedly rose +0.1 to 8.5, better than expectations of-0.3 to 8.0, and (2) concern that the spread of the Ebola virus may undercut economic growth and prompt the Fed to delay any interest rate hikes after New York City reported its first case of the virus.

Dec WTI crude oil (CLZ14 -0.52%) this morning is down -43 cents (-0.53%) and Dec gasoline (RBZ14 -0.48%) is down -0.0187 (-0.87%). Dec crude and Dec gasoline on Friday closed lower. Closes: CLZ4 -1.08 (-1.32%), RBZ4 -0.0238 (-1.10%). Negative factors included (1) speculation that Saudi Arabia won’t cut crude production in an attempt to push oil prices higher as they try to keep their share of OPEC output, and (2) concern that the spread of the Ebola virus may undercut consumer sentiment and spending and lead to slower economic growth and energy demand after the first case of the Ebola virus was reported in New Your City.

Disclosure: None