Morning Call For Sept. 24, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 +0.25%) this morning are up +0.25% and European stocks are up +0.41% ahead of U.S. economic data on Aug new home sales that are expected to post an increase. Gains in European stocks were limited after German business confidence fell for a fifth month to the lowest in 17 months. Asian stocks closed mixed: Japan -0.24%, Hong Kong +0.35%, China +1.77%, Taiwan +0.15%, Australia -0.74%, Singapore -0.16%, South Korea +0.15%, India -0.12%. China's Shanghai Stock Index climbed to a 1-week high and closed higher on a rally in brokerage stocks and defense companies. Brokerages gained after data from the China Securities Depository and Clearing showed Chinese investors opened 217,000 new trading accounts last week, the most in 2 years, amid speculation an exchange link with Hong Kong will boost trading. The exchange link with Hong Kong will start next month and allow a net 23.5 billion yuan ($3.8 billion) of daily cross-border stock purchases. Chinese defense companies moved higher on speculation of increased state spending after China's President Xi Jinping called on the People's Liberation Army (PLA) to boost their combat readiness. Commodity prices are mixed. Nov crude oil (CLX14 -0.15%) is down -0.16%. Nov gasoline (RBX14 -0.66%) is down -0.45%. Dec gold (GCZ14 -0.05%) is up +0.05%. Dec copper (HGZ14 +0.08%) is up +0.15%. Agriculture and livestock prices are mostly higher. The dollar index (DXY00 +0.13%) is up +0.02%. EUR/USD (^EURUSD) is down -0.04%. USD/JPY (^USDJPY) is down -0.17%. Dec T-note prices (ZNZ14 -0.05%) are down -2 ticks.

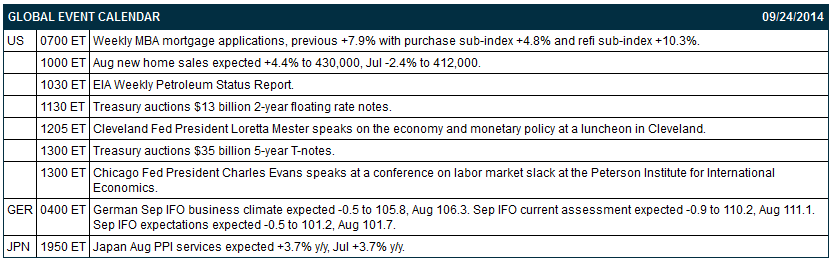

The German Sep IFO business climate fell -1.6 to 104.7, a bigger decline than expectations of -0.5 to 105.8 and the lowest in 17 months.

Kansas City Fed President George said that the economy is moving forward "on about a 3% trajectory" and that interest rates "should have been off zero by this point." She added that the Fed should raise rates gradually and systematically and that its balance sheet should revert to holding Treasuries only.

The Japan Sep Markit/JMMA manufacturing PMI fell -0.5 to 51.7.

U.S. STOCK PREVIEW

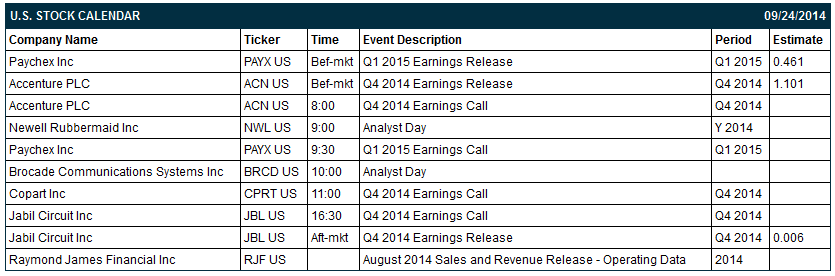

Today’s Aug new home sales report is expected to show an increase of +4.4% to 430,000, more than reversing July’s decline of -2.4% to 412,000. The Treasury today will sell $13 billion of 2-year floating-rate notes and $35 billion of 5-year T-notes. The Treasury will then conclude this week’s $106 billion T-note auction package by selling $29 billion of 7-year T-notes on Thursday. There are three of the Russell 1000 companies that report earnings today: Paychex (consensus $0.46), Accenture (1.10), Jabil Circuit (0.01). Equity conferences during the remainder of this week include: World LNG Series:Asia Pacific Summit on Tue-Thu, Avondale's Dallas Airlines Day on Wed, and 8th Rocky Mountain Utility Efficiency Exchange on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

Rio Tinto (RIO +1.51%) was upgraded to 'Overweight' from 'Equal Weight' at Morgan Stanley.

Ericsson (ERIC -1.46%) was downgraded to 'Neutral' from 'Buy' at UBS.

Accenture PLC (ACN +0.48%) reported Q4 EPS of $1.08, below consensus of $1.10.

Autoliv (ALV -0.98%) was initiated with an 'Outperform' at Exane BNP Paribas with a price target of $118.

Morgan Stanley (MS -0.45%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Sage Therapeutics (SAGE +11.55%) was upgraded to 'Buy' from 'Neutral' at Goldman Sachs.

Newmont Mining (NEM +1.39%) raised its 2014 copper output guidance to 120,000 metric tons MT-125,000 MT from 80,000 MT-95,000 MT and raised its fiscal year 2015 copper production guidance to 250,000 MT-270,000 MT from 220,000 MT-240,000 MT following the receipt of an export permit in Indonesia.

Bed Bath & Beyond (BBBY -1.57%) jumped over 6% in after-hours trading after it reported Q2 EPS of $1.17, better than consensus of $1.14.

AAR Corp. (AIR +0.25%) reported Q1 EPS of 36 cents, less than consensus of 38 cents, and then lowered guidance on fiscal 2015 EPS view to $1.65-$1.75 from $1.80-$1.90, below consensus of $1.87.

Steelcase (SCS +0.19%) reported Q2 adjusted EPS of 27 cents, higher than consensus of 23 cents.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 +0.25%) this morning are up +5.00 points (+0.25%). The S&P 500 index on Tuesday closed lower: S&P 500 -0.58%, Dow Jones-0.68%, Nasdaq -0.24%. Bearish factors included (1) an escalation of the Middle East conflict after the U.S. and its Arab allies began airstrikes on ISIS positions in Syria, (2) the +0.1% increase in the Jul FHFA house price index, weaker than expectations of +0.5%, and (3) weakness in health-care stocks on concern the action by the Treasury Department to crack down on tax-saving mergers will hurt M&A activity in the health-care sector.

Dec 10-year T-notes (ZNZ14 -0.05%) this morning are down -2 ticks. Dec 10-year T-note futures prices on Tuesday closed higher. Supportive factors included (1) the smaller-than-expected increase in Jul FHFA home prices, and (2) increased safe-haven demand from geopolitical risks in the Middle East after the U.S began airstrikes in Syria and after Israel shot down a Syrian fighter plane that had infiltrated Israeli airspace. Closes: TYZ4 +8.00, FVZ4 +4.00.

The dollar index (DXY00 +0.13%) this morning is up +0.013 (+0.02%). EUR/USD (^EURUSD) is down -0.0005 (-0.04%) and USD/JPY (^USDJPY) is down-0.19 (-0.17%). The dollar index on Tuesday closed lower. Negative factors included (1) increased safe-haven demand for the yen after the U.S. and its Arab allies launched airstrikes against Islamic militants in Syria, and (2) the smaller-than-expected increase in Jul FHFA home prices. Strength in EUR/USD was limited after the Eurozone Sep Markit manufacturing PMI fell more than expected to the slowest pace of expansion in 14 months. Closes: Dollar index -0.094 (-0.11%), EUR/USD -0.0002 (-0.01%), USD/JPY +0.05 (+0.05%).

Nov WTI crude oil (CLX14 -0.15%) this morning is down -15 cents (-0.16%) and Nov gasoline (RBX14 -0.66%) is down -0.0113 (-0.45%). Nov crude and gasoline prices on Tuesday closed higher: CLX4 +0.69 (+0.76%), RBXX4 +0.0139 (+0.56%). Bullish factors included (1) reduced Chinese economic concerns after the China Sep HSBC manufacturing PMI unexpectedly rose, (2) the weaker dollar, and (3) geopolitical concerns in the Middle East after the U.S. and its Arab allies launched airstrikes against the Islamic State in Syria and after Israel shot down a Syrian fighter plane that penetrated Israeli airspace.

Disclosure: None