Morning Call For Sept. 4, 2014

OVERNIGHT MARKETS AND NEWS

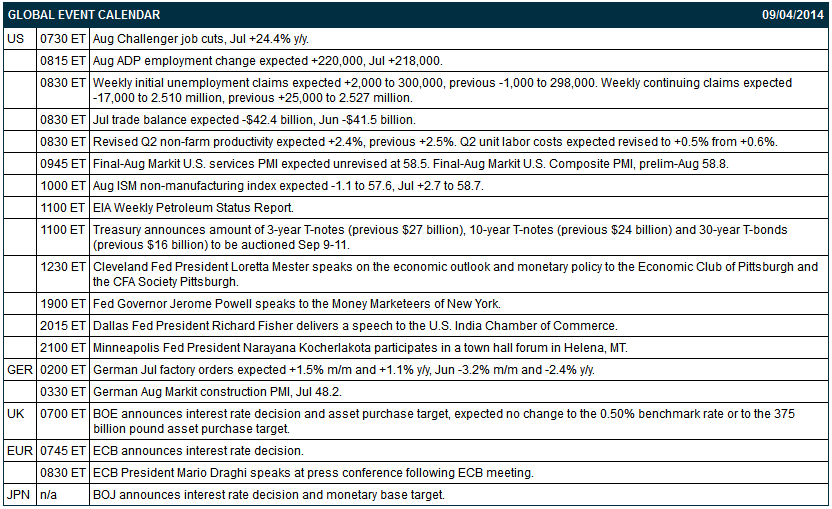

September E-mini S&Ps (ESU14 +0.31%) this morning are up +0.24% on optimism that this morning's ADP employment report will show solid gains in employment last month, while European stocks are little changed ahead of the results of today's ECB meeting. A positive for European stocks was the largest increase in German factory orders in 13 months. As expected, the BOE kept its benchmark rate at 0.50% and maintained its asset purchase target at 375 billion pounds. Asian stocks closed mixed: Japan -0.33%, Hong Kong -0.08%, China +0.72%, Taiwan -0.23%, Australia -0.44%, Singapore -0.07%, South Korea +0.35%, India -0.20%. China's Shanghai Stock Index climbed to a 1-1/4 year high on signs the government is boosting stimulus measures after Reuters reported that Chinese regulators will allow property developers to issue mid-term notes in the interbank market to cut funding costs. Commodity prices are mixed. Oct crude oil (CLV14 -0.24%) is down -0.40%. Oct gasoline (RBV14 +0.48%) is up +0.19%. Dec gold (GCZ14 +0.06%) is up +0.15%. Dec copper (HGZ14 +0.88%) is up +0.58%. Agriculture and livestock prices are mixed with Dec wheat down -0.70% at a new contract low and Oct cattle up +1.58% at a 5-week high. The dollar index (DXY00 +0.08%) is up +0.14%. EUR/USD (^EURUSD) is down -0.18%. USD/JPY (^USDJPY) is up +0.19%. Dec T-note prices (ZNZ14 -0.05%) are up +0.5 of a tick.

The BOJ said it will maintain record stimulus following its 2-day policy meeting as it kept its pledge to increase the monetary base at an annual pace of 60 trillion to 70 trillion yen ($667 billion). BOJ Governor Kuroda said a moderate recovery would continue and indicated a weaker yen would support the Japanese economy that still faces headwinds from the Apr sales tax hike.

German Jul factory orders rose +4.6% m/m, more than expectations of +1.5% m/m and the largest monthly increase in 13 months. On an annual basis, Jul factory orders rose +4.9% y/y, stronger than expectations of +1.1% y/y.

U.S. STOCK PREVIEW

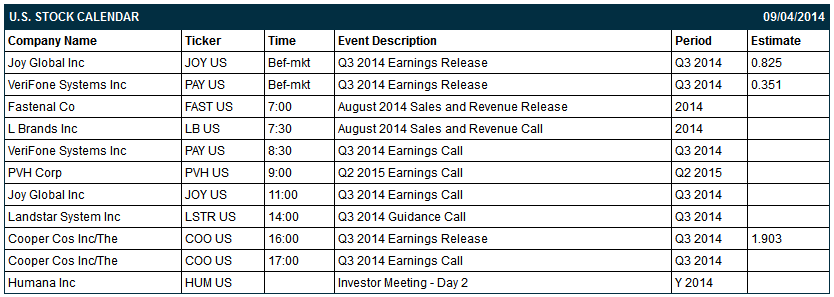

The market is expecting today’s Aug ADP employment report to show another solid increase of +220,000, improving slightly from +218,000 in July. The market is expecting today’s initial unemployment claims report to show a small +2,000 increase to 300,000 following last week’s -1,000 decline to 298,000. The market is expecting today’s July U.S. trade deficit to widen mildly to -$42.4 billion from -$41.5 billion in June. The market is expecting today’s Aug ISM non-manufacturing index to show a -1.1 point decline to 57.6, reversing part of the +2.7 point increase to 58.7 seen in July. There are three of the Russell 1000 companies that report earings today: Joy Global (consensus: $0.83), VeriFone (0.35), Cooper Cos. (1.90).

Equity conferences during the remainder of this week include: Citi Global Technology Conference on Tue-Thu, Barclays CEO Energy-Power Conference on Tue-Thu, Drexel Hamilton Telecom, Media, and Technology Conference on Wed-Thu, KBW Insurance Conference on Wed-Thu, Robert W. Baird & Co Health Care Conference on Wed-Thu, Barclays Back to School Conference on Wed-Fri, Vertical Research Partners Industrial Conference on Wed-Fri, Mizuho Investment Conference on Thu, Bloomberg Sports Business Summit on Thu, Citi Biotech Conference on Thu, Nomura Digital Media Conference on Thu, Renewable Energy India Expo 2014 on Thu, and Scotia Capital, Inc Financial Summit on Thu.

OVERNIGHT U.S. STOCK MOVERS

VeriFone (PAY -1.31%) reported Q3 EPS of 40 cents, stronger than consensus of 35 cents, and then raised guidance on fiscal 2014 EPS view to $1.46-$1.47, above consensus of $1.45.

L Brands (LB +0.13%) reported August sales up 9% and same-store-sales up 5%.

Las Vegas Sands (LVS +0.70%) was downgraded to 'Hold' from 'Buy' at Argus.

Ciena (CIEN +1.49%) reported Q3 adjusted EPS of 32 cents, better than consensus of 29 cents.

D.R. Horton (DHI -2.54%) was upgraded to 'Buy' from 'Neutral' at UBS.

Foot Locker (FL -0.23%) was initiated with a 'Buy' at Jefferies with a price target of $66.

Joy Global (JOY -0.58%) reported Q3 EPS of 80 cents, weaker than consensus of 84 cents.

Yum! Brands (YUM +0.08%) slid over 3% in after-hours trading after it said it sees its Q3 China division same-store-sales down 13% versus prior year.

Weyerhaeuser (WY -0.29%) was initiated with an 'Outperform' at BMO Capital with a price target of $39.

Symantec (SYMC +0.04%) rose almost 1% in after-hours trading after Bloomberg reported that it is working with Home Depot on its data breach.

ABM Industries (ABM -0.67%) reported Q3 adjusted EPS of 47 cents, better than consensus of 46 cents, and then raised guidance on fiscal 2014 adjusted EPS view to $1.65-$1.69, higher than consensus of $1.60.

Matrix Service (MTRX +2.53%) reported Q4 EPS of 28 cents, below consensus of 36 cents, and then lowered guidance on fiscal 2015 EPS to $1.40-$1.60, well below consensus of $1.77.

WhiteWave Foods (WWAV -1.67%) was initiated with an 'Outperform' at Oppenheimer with a price target of $43.

PVH Corp. (PVH +0.69%) jumped 5% in after-hours trading after it reported Q2 EPS of $1.51, above consensus of $1.42.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 +0.31%) this morning are up +4.75 points (+0.24%). The S&P 500 Index on Wednesday fell back from a new record high and closed lower as weakness in technology stocks dragged the overall market lower after Apple slumped when Samsung introduced new smartphones: S&P 500 -0.08%, Dow Jones +0.06%, Nasdaq -0.61%. The S&P 500 had posted a new record high on bullish factors that included (1) reduced tensions in Ukraine after Russian and Ukrainian leaders agreed on a framework for a cease fire, and (2) the +10.5% increase in U.S. Jul factory orders, although less than expectations of +10.8%, was still the largest monthly gain since the data series began in 1956.

Dec 10-year T-notes (ZNZ14 -0.05%) this morning are up +0.5 of a tick. Dec 10-year T-note futures prices on Wednesday fell to a 3-week low on reduced safe-haven demand when the S&P 500 surged to a record high after Russian and Ukrainian leaders agreed on steps toward a cease-fire in eastern Ukraine. However, T-note prices recovered and closed unchanged after stocks fell back from their best levels along with skepticism over Russia's resolve to end the conflict after Ukraine Prime Minister Yatsenyuk sad Russia has "cheekily violated" all previous agreements. Closes: TYZ4 unch, FVZ4 -0.25.

The dollar index (DXY00 +0.08%) this morning is up +0.115 (+0.14%). EUR/USD (^EURUSD) is down -0.0024 (-0.18%) and USD/JPY (^USDJPY) is up +0.20 (+0.19%). The dollar index on Wednesday fell back from a 13-1/2 month high and closed lower. Bearish factors included (1) reduced geopolitical tensions that undercut safe-haven demand for the dollar after Russian and Ukrainian leaders agreed on steps toward a cease-fire in eastern Ukraine, and (2) short-covering in EUR/USD ahead of Thursday's monthly ECB meeting. Closes: Dollar index -0.127 (-0.15%), EUR/USD +0.00175 (+0.13%), USD/JPY -0.305 (-0.29%).

Oct WTI crude oil (CLV14 -0.24%) this morning is down -38 cent (0.40%) and Oct gasoline (RBV14 +0.48%) is up +0.0049 (+0.19%). Oct crude and gasoline prices on Wednesday closed higher: CLV4 +2.66 (+2.86%), RBV4 +0.0770 (+3.03%). Bullish factors included (1) reduced tensions in Ukraine after Ukraine President Poroshenko and Russian President Putin discussed a plan for a cease-fire, which boosted speculation that sanctions against Russia will ease and may boost European economic growth, and (2) expectations for Thursday's weekly EIA data will show crude supplies fell -1.0million bbl, the third consecutive decline.

Disclosure: None