Morning Call For Sept. 9, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 +0.07%) this morning are up +0.02% and European stocks are down -0.26%. The EU's second package of economic sanctions against Russia was put on hold for a "few days" to allow for more time to assess the viability of a cease-fire and a peace plan in Ukraine, according to EU President Van Rompuy. Losses in European stocks were limited and the British pound recovered from a 9-1/2 month low against the dollar after UK Aug industrial production rose more than expected. GBP/USD also received support from comments from BOE Governor Carney who said "the point at which interest rates also begin to normalize is getting closer." Asian stocks closed mixed: Japan +0.28%, Hong Kong and South Korea closed for holiday, China -0.16%, Taiwan +0.29%, Australia +0.55%, Singapore +0.23%, India -0.20%. Japanese exporters rallied and led the Nikkei Stock Index higher after the yen slumped to a 5-3/4 year low against the dollar, which boosts the earnings prospects of exporters. Commodity prices are mixed. Oct crude oil (CLV14 +1.36%) is up +0.85%. Oct gasoline (RBV14 +0.30%) is down -0.25%. Dec gold (GCZ14 +0.21%) is up +0.20%. Dec copper (HGZ14-0.79%) is down 0.79%. Agriculture and livestock prices are mixed. The dollar index (DXY00 +0.12%) is up +0.09% at a new 13-3/4 month high. EUR/USD (^EURUSD) is down -0.07% at a 13-3/4 month low. USD/JPY (^USDJPY) is up +0.15% at a 5-3/4 year high. Dec T-note prices (ZNZ14 -0.28%) are down-10 ticks.

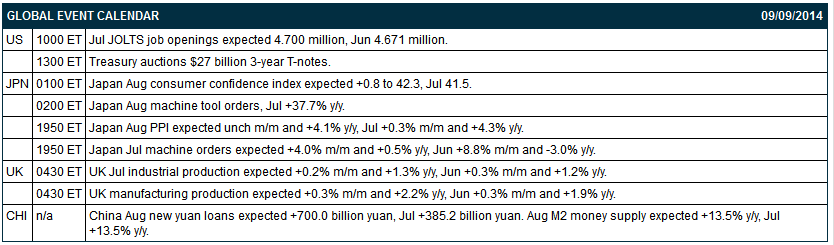

UK Aug industrial production rose +0.5% m/m and +1.7% y/y, better than expectations of +0.2% m/m and +1.3% y/y. Aug manufacturing production rose +0.3% m/m and +2.2% y/y, right on expectations.

Japan Aug consumer confidence unexpectedly fell -0.3 to 41.2, weaker than expectations of +0.8 to 42.3.

Japan Aug machine tool orders rose +35.6% y/y, the eleventh consecutive month of year-over-year increases.

The Japan Jul tertiary industry index was unchanged m/m, weaker than expectations of +0.2% m/m.

U.S. STOCK PREVIEW

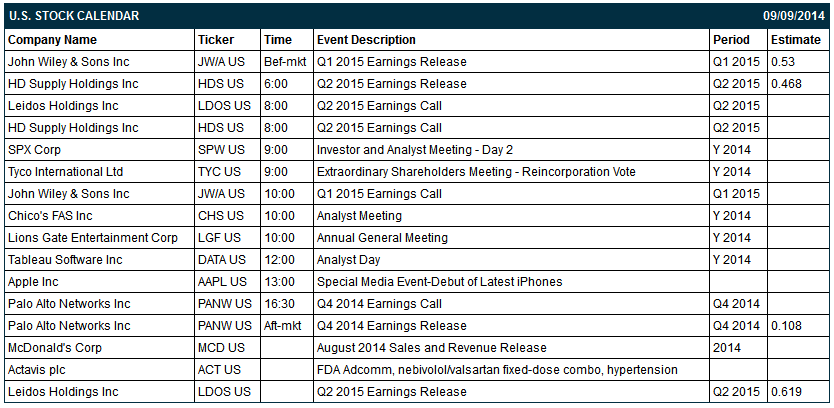

Today’s July JOLTS U.S. job openings report is likely to post a new 13-1/3 year high of 4.7 million, an indication that the supply of new unfilled jobs has reached the highest level since February 2001. The Treasury today will sell $27 billion of 3-year T-notes, kicking off this week’s $61 billion coupon package. There are four Russell 1000 companies that report earnings today: John Wiley & Sons (consensus: $0.53), HD Supply Holdings 0.47, Palo Alto Networks 0.11 and Leidos Holdings 0.62.

Equity conferences the rest of this week include: Morgan Stanley Healthcare Conference on Mon-Wed, Barclays Global Financial Services Conference on Mon-Wed, D.A. Davidson Engineering & Construction Conference on Tue, KeyBanc Capital Markets Basic Materials & Packaging Conference on Tue, 4G World 2014/Tower & Small Cell Summit on Tue, Gabelli & Company Aerospace Conference on Tue, Gabelli Aircraft Suppliers Conference on Tue, Raymond James North American Equities Conference on Tue, Deutsche Bank dbAccess Technology Conference on Tue-Wed, RBC Capital Market Global Industrials Conference on Tue-Wed, UBS Best of Americas Conference on Tue-Thu, Latin Markets Mexico Energy Summit on Wed, Pareto Oil & Offshore Conference on Wed, Longbow Research - Industrial Manufacturing & Technology Investor Conference on Wed, Goldman Sachs Communacopia Conference on Wed-Fri, UBS Global Paper & Forest Products Conference on Thu, BIO Latin America Conference on Thu, and Credit Suisse Asian Technology Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Ralph Lauren (RL -0.23%) was upgraded to 'Strong Buy' from 'Buy' at ISI Group.

Total (TOT -2.26%) was upgraded to 'Neutral' from 'Underperform' at BofA/Merrill.

HD Supply (HDS -0.83%) reported Q2 adjusted EPS of 51 cents, better than consensus of 47 cents.

Leidos (LDOS -0.89%) reported Q2 EPS of 61 cents, less than consensus of 62 cents, and then lowered guidance on fiscal 2015 EPS view to $2.10-$2.30 from $2.35-$2.55, well below consensus of $2.47.

Dick's Sporting Goods (DKS -0.46%) was downgraded to 'Market Perform' from 'Outperform' at Wells Fargo.

The U.S. airline sector, which includes United Continental (UAL +0.79%), Delta Air Lines (DAL -0.46%) and American Airlines (AAL +1.00%), were initiated with an 'Overweight' at Credit Suisse.

D.R. Horton (DHI +0.75%) and Lennar (LEN +0.44%) were both upgraded to 'Overweight' from 'Neutral' at JPMorgan.

Annie's (BNNY -1.12%) surged over 30% in after-hours trading after General Mills (GIS -0.58%) said it will buy the company for $46 per share in cash or about $820 million.

Pep Boys (PBY +1.97%) dropped over 6% in after-hours trading afte rit reported Q2 EPS of 0 cents with items, well below consensus of 16 cents.

CHC Group (HELI -1.89%) reported a Q1 EPS loss of -46 cents, less than consensus of -47 cents.

Casey's General Stores (CASY -0.54%) rose over 3% in after-hours trading after it reported Q1 EPS of $1.43, well above consensus of $1.24.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 +0.07%) this morning are up +0.50 of a point (+0.02%). The S&P 500 Index on Monday closed lower: S&P 500 -0.31%, Dow Jones -0.15%, Nasdaq +0.14%. Negative factors included (1) Chinese economic concerns after China Aug imports unexpectedly fell -2.4% y/y, weaker than expectations of +3.0% y/y and the biggest decline in 5 months, and (2) European economic concerns after the Eurozone Sep Sentix investor confidence dropped -12.5 points to -9.8, a bigger decline than expectations of -1.3 to 1.4 and the lowest in 14 months.

Dec 10-year T-notes (ZNZ14 -0.28%) this morning are down -10 ticks. Dec 10-year T-note futures prices on Monday closed lower. The main bearish factor for T-note prices is supply pressures with the Treasury set to auction $61 billion of T-notes and T-bonds this week starting with Tuesday's $27 billion auction of 3-year T-notes. Losses were limited after Morgan Stanley reduced its year-end 10-year T-note yield forecast to 2.85% from 3.00%, citing global geopolitical concerns and weakness in the European growth outlook. Closes: TYZ4 -3.50, FVZ4 -4.75.

The dollar index (DXY00 +0.12%) this morning is up +0.078 (+0.09%) at a new 13-3/4 month high. EUR/USD (^EURUSD) is down -0.0009 (-0.07%) at a 13-3/4 month low and USD/JPY (^USDJPY) is up +0.16 (+0.15%) at a fresh 5-3/4 year high. The dollar index on Monday surged to a 13-3/4 month high and closed higher. Bullish factors included (1) weakness in EUR/USD which slumped to a 13-3/4 month low after the Eurozone Sep Sentix investor confidence fell more than expected to a 14-month low, and (2) a surge in USD/JPY to a 5-3/4 year high as the yen plunged against the dollar on signs the Japanese economy is weaker than anticipated after Japan Q2 GDP was revised lower to -7.1% q/q annualized, the biggest pace of contraction in 5 years. Closes: Dollar index +0.493 (+0.59%), EUR/USD -0.0054 (-0.42%), USD/JPY +0.989 (+0.94%).

Oct WTI crude oil (CLV14 +1.36%) this morning is up +79 cents (+0.85%) and Oct gasoline (RBV14 +0.30%) is down -0.0064 (-0.25%). Oct crude and gasoline prices on Monday closed lower for a third day with Oct crude at a 7-3/4 month low and Oct gasoline at a 2-1/2 week low: CLV4 -0.63 (-0.68%), RBV4 -0.0184 (-0.71%). Bearish factors included (1) the rally in the dollar index to a 13-3/4 month high, and (2) Chinese demand concerns after China Aug imports unexpectedly fell by the most in 5 months.

Disclosure: None