Oil & Dollar At Crucial Long-Term Areas – Weekly Market Outlook

While the release of the Federal Reserve's meeting minutes on Wednesday of last week was supposed to be catalytic, the market seemed a little disappointed – and disinterested – in the fact that Janet Yellen and her cohorts didn't really say much (or decide much) of anything during last month's gathering. It wasn't until Friday's news that Europe as well as China would be issuing new stimulus that we saw U.S. stocks start to move. But, move they did, with the S&P 500 (SPX) (SPY) hitting record highs in the process.

The overall trend for stocks remains positive, for the time being. We'll take a look at the bigger market picture right after we take a closer look at last week's economic reports. Lastly, we look at the big picture view of Crude Oil and the Dollar Index, both of which are around possible reversal areas.

Economic Data

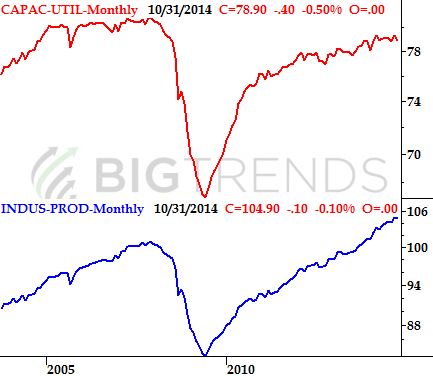

We worked our way through a pretty big dose of economic information last week, and it was mostly good. We didn't start the week out on the strongest foot though, with less-than-stellar industrial production and capacity utilization numbers. Industrial production numbers fell 0.1% in October, and capacity utilization fell from 79.2% to 78.9%.

As our chart indicates, neither lull is a trend-breaker. On the other hand, no trend is dramatically big when it first develops.

Industrial Productivity & Capacity Utilization Chart

Source: Federal Reserve

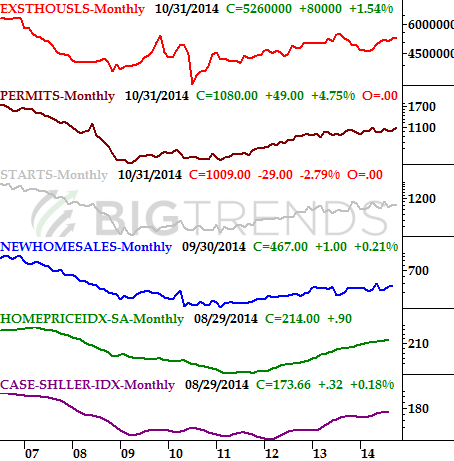

From that point forward, the news turned relatively encouraging, especially for real estate. The NAHB Housing Market Index rose from 54 to 58 for November, and existing home sales reached a new multi-month high pace of 5.26 million. Housing starts for October fell from September's pace, but the 1.009 million units is still solid. Building permits grew from 1.031 million to 1.080 million units for last month. The bigger trend remains positive.

Real Estate Trends Chart

Source: Census Bureau, National Assn. of Realtors, Standard & Poor's, and FHFA

There's more data on the way this week to round out the picture, but barring some surprising weakness on the yet-to-be-released numbers, we have to continue to view real estate and construction in a positive light.

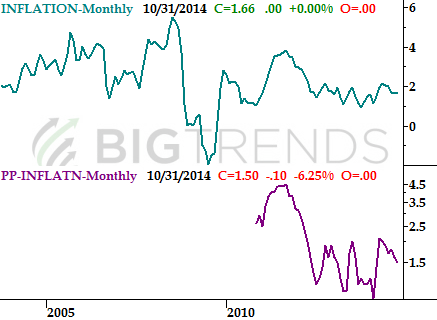

Finally, we also got an updated view of the inflation picture last week. As of October, the annualized consumer inflation rate stands at 1.66% (same as September), while the producer price inflation rate fell from 1.6% to 1.5%. The tumble of oil and gasoline prices, and food prices, was the core of the reason for the lull. It's not deflation yet, but the Federal Reserve was understandably concerned about weak – and weakening – inflation, as indicated by last week's release of last month's Fed meeting minutes.

Inflation Chart

Source: Bureau of Labor Statistics

Although the Fed didn't "do" anything to stave off the likely slide of already-weak inflation that will be caused by the end of its bond-buying/QE efforts and the eventual rise in interest rates, it's clearly on Janet Yellen's radar.

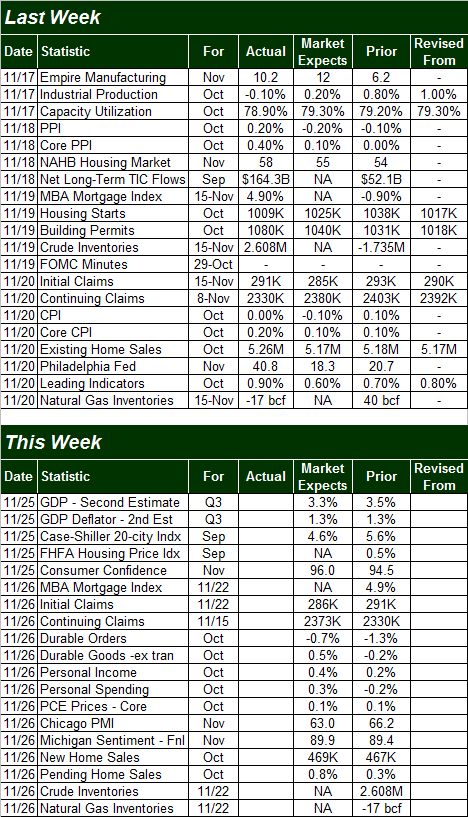

Everything else is on the following grid:

Economic Calendar

Source: Briefing.com

Stock Market Index Analysis

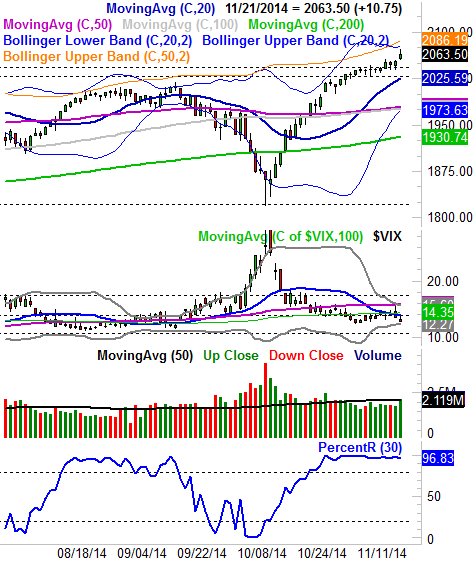

The daily chart below of the S&P 500 speaks for itself. The index wiggled and writhed its way above a ceiling at 2044 early last week, and then picked up the pace of buying on Friday when both China and Europe decided their economies needed more stimulus. Regardless of the reason, the news breathed some new life into the rally that extends all the way back to the October 15th low.

S&P 500 & VIX – Daily Chart

All charts created with TradeStation

For what it's worth, notice the Williams Percent R indicator (using the BigTrends smoothed method on it of 30 input) never slipped back under the key 80 level after moving above it on October 28th. This isn't surprising. While the market was arguably vulnerable to a pullback by early November, we never got any actual evidence that a pullback was unavoidable; the signal would have been a PercentR line falling under 80. And, it's also worth noting the Percent R indicator was also persistently -and accurately – bullish in August and early September. Once the Percent R line did make a sustained break under 80 in September, it still happened well in advance of the bulk of the selloff later in the month.

It's also worth adding we saw a bit of a volume bump behind Friday's advance.

The rally isn't bulletproof, of course – a couple of tripwires lie ahead. One of them is resistance at 2077 where the upper 20-day Bollinger band lines. The 50-day Bollinger band at 2086 could also slow the rally down. Just for the record, however, bumping into the upper band lines doesn't inherently mean the S&P 500 has to pull back. The upper Bollinger bands could end up simply guiding the index higher indefinitely.

The low CBOE Volatility Index (VIX) (VXX) is also a potential problem, as a low VIX reading is often an indication of too much complacency, which generally leads to a market top. Even so, we only have to look back to August and September to see the VIX can remain at low readings for a while, and stocks rally the whole time.

Whatever the case, there's major support developing at 2029. That was a floor two weeks ago, and that's where the 20-day moving average line will be by the end of this week. Should that support level fail to hold up, the next big one is at 1975, where the 100-day and 50-day moving average lines are converging with the lower 20-day Bollinger band. First things first though.

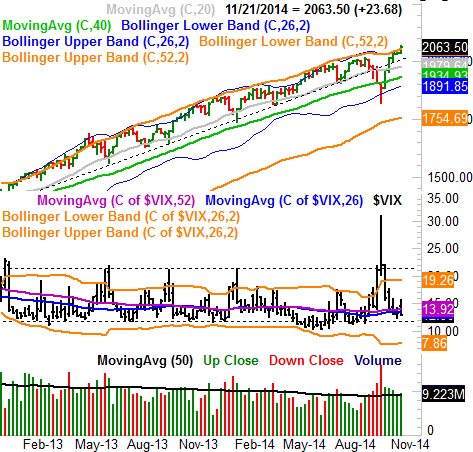

The weekly chart doesn't tell us anything new. It does, however, remind us that the S&P 500 is still in the midst of a long-term uptrend, and that a rising floor at 2014 (dashed) is still in play. The weekly chart is also a reminder the VIX is comfortable getting to – and falling back to – the 12 area. We only need to get really worried if the VIX starts to trend higher in this timeframe. What we saw in October was hardly a trend.

S&P 500 & VIX - Weekly Chart

Commodities & Sectors: Oil Near Crucial Support Areas, Dollar Near Long Term Resistance

As you can see on the long-term charts below, Crude Oil (USO) has dropped sharply to possible support areas. Similarly, the Dollar Index (UUP) is reaching potential resistance. So be aware that these strong trends could reverse quickly — but they haven't been broken yet.

When crude prices plunged severely and the wedge pattern was broke in September, oil fell all the way to a low of $73.22 two weeks ago — that was right around the floor defined near that area with lows hit in 2011 and 2012, and the $72.67 line is a 50% retracement of the entire swing we saw from crude oil in 2008. 50% retracements of trends are often important reversal areas (and are a part of Fibonacci analysis). So this is a logical area for Oil to possibly bottom out.

Crude Oil – Weekly Chart (with U.S. Dollar Index)

It's also possible the U.S. dollar's rally could be running out of steam at a logical place. As the chart illustrates, there's a natural ceiling for the U.S. Dollar Index at 88.6, and the uptrend has slowed for a couple weeks now just below that mark. The world is clearly hesitant. Just bear in mind that the dollar isn't the only thing that affects the price of oil, but It's a significant factor at times.

Disclosure: None.

Comments

No Thumbs up yet!

No Thumbs up yet!