Our Marginal Economy

Before you jump on the Bull market bandwagon of "don't fight the Fed," perhaps you should take a look at the quality of the debt the Fed has enabled and the diminishing returns on all that debt.

The mainstream media is delighted to highlight positive economic data, but nobody ever asks about the quality of the borrowers who are behind the rosy numbers. Behind the rosy numbers, sales and profits are increasingly dependent on marginal buyers and borrowers: those buying on credit who would not qualify to borrow money in a system ruled by prudent risk-management.

These marginal borrower/buyers are last on, first off: they qualify for loans at the end of a credit expansion, when lenders throw caution to the winds to reap the profits from issuing new mortgages, auto loans, student loans, credit cards, etc. to marginal borrowers.

These marginal borrowers are the first to default, because they have insufficient income and collateral to support their loans.

This rising dependence on marginal borrowers/buyers leads to an economy of diminishing returns: ever-rising rates of debt expansion are required to generate ever-declining rates of expansion of sales, profits, GDP, etc.

The waterfall decline of the quality of debt-based sales is masked by the rosy headline numbers. Auto sales are soaring; nice, but does anyone ask how many of those vehicles were sold to marginal buyers, the kind of borrowers who are one paycheck away from insolvency and default?

How many issuers of junk bonds are one recession away from insolvency and default?

Let's look at a few examples of diminishing returns/dependence on rising debt for marginal returns. Once again, we must keep in mind the quality of the debt and the borrowers is not revealed in rosy headline numbers.

Anecdotally, I see plenty of people who defaulted/declared bankruptcy in previous downturns who are once again in hock to the hilt, and they know the drill: borrow and spend as much as you can, because all you have to do is stop paying.

Yes, your credit score will be lousy for a few years, but lenders and retailers are so desperate for sales that you won't have to wait long to start getting a flood of credit card offers in your mailbox. After all, anyone with a pulse can buy a car now.

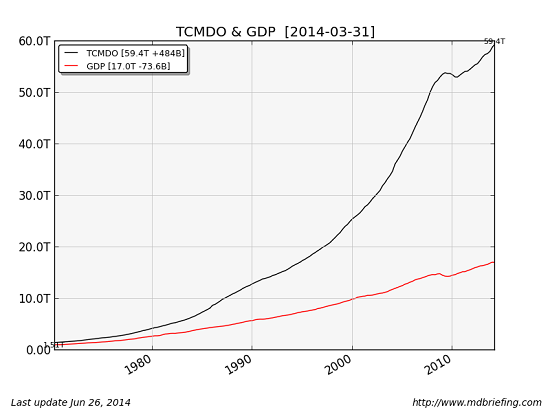

Here's total credit and GDP: this screams "diminishing returns":

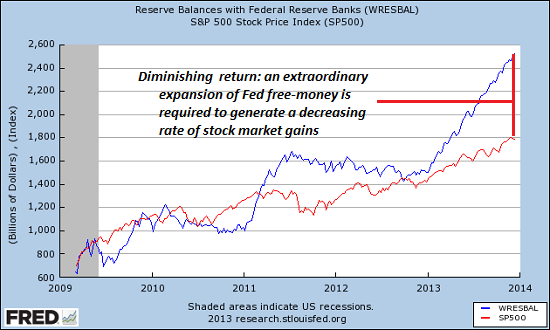

The Fed's "free-money for financiers" balance sheet and the S&P 500: once again, this screams "diminishing returns:"

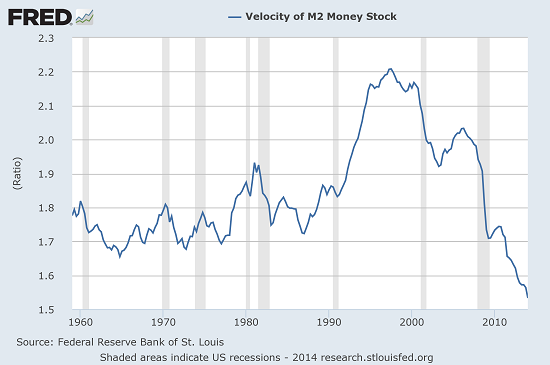

Money velocity: diminishing returns:

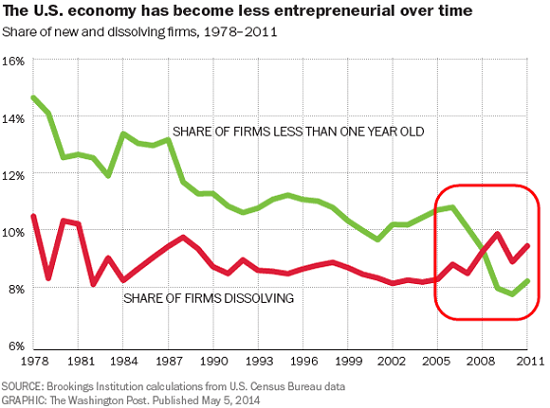

Small biz: fading at the margins:

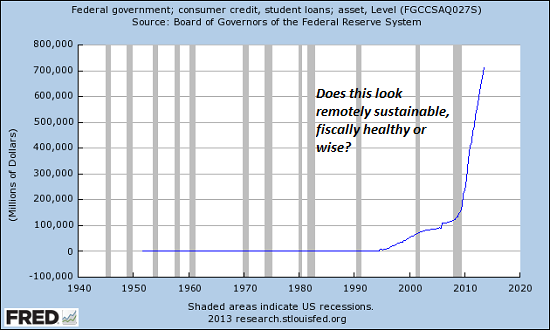

Federal student loans: this fairly screams, "go ahead and default, there is literally no risk management here":

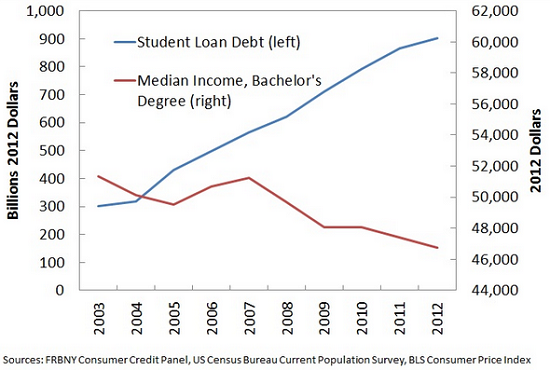

The return on a college degree? Diminishing faster than you can say "default":

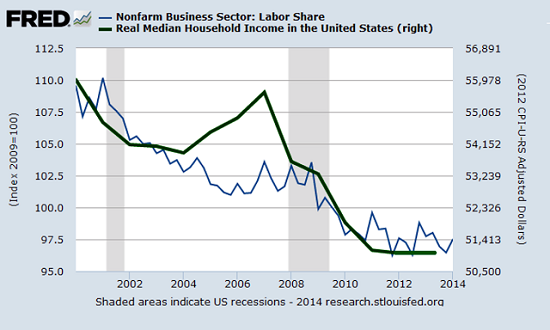

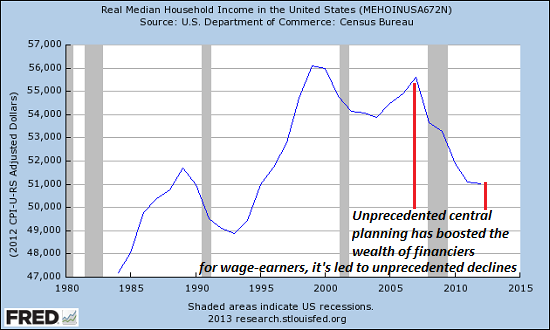

Labor participation and real median income: diminishing returns on all the outlandish money pumping and Federal deficit spending:

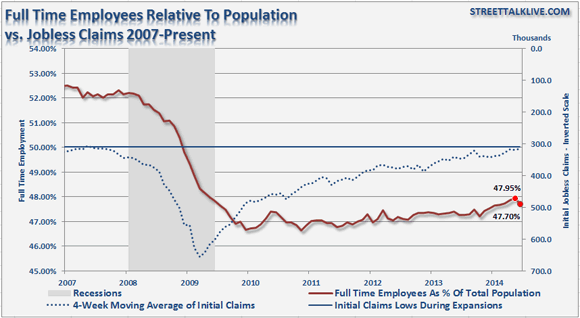

Fulltime employment: going nowhere after 5+ years of unprecedented expansion of central bank "free money for financiers" and Federal debt:

Real household income: declining for all but the top 5%:

Household income has declined significantly in real terms: Five Decades of Middle Class Wages (Doug Short).

Federal Reserve "free money for financiers" has greatly expanded wealth inequality:

So before you jump on the Bull market bandwagon of "don't fight the Fed," perhaps you should take a look at the quality of the debt the Fed has enabled and the diminishing returns on all that debt.

None.