Personal Consumption Expenditures: October 2014 Preview

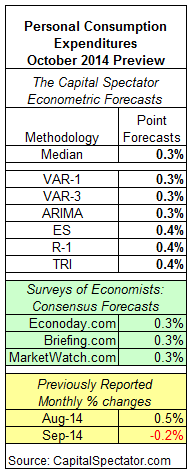

US personal consumption spending for October is projected to rise 0.3% vs. the previous month in tomorrow’s update (Nov. 26), based on The Capital Spectator’s median point forecast for several econometric estimates. The prediction reflects a moderate rebound in growth relative to September’s 0.2% decline.

Compared with a trio of consensus estimates based on recent surveys of economists, The Capital Spectator’s median forecast for October matches the projections.

Here’s a closer look at the numbers, followed by brief summaries of the methodologies behind the forecasts that are used to calculate The Capital Spectator’s median prediction:

VAR-1: A vector autoregression model that analyzes the history of personal income in context with personal consumption expenditures. The forecasts are run in R with the “vars” package.

VAR-3: A vector autoregression model that analyzes three economic time series in context with personal consumption expenditures. The three additional series: US private payrolls, personal income, and industrial production. The forecasts are run in R with the “vars” package.

ARIMA: An autoregressive integrated moving average model that analyzes the historical record of personal consumption expenditures in R via the “forecast” package to project future values.

ES: An exponential smoothing model that analyzes the historical record of personal consumption expenditures in R via the “forecast” package to project future values.

R-1: A linear regression model that analyzes the historical record of personal consumption expenditures in context with retail sales. The historical relationship between the variables is applied to the more recently updated retail sales data to project personal consumption expenditures. The computations are run in R.

TRI: A model that’s based on combining point forecasts, along with the upper and lower prediction intervals (at the 95% confidence level), via a technique known as triangular distributions. The basic procedure: 1) run a Monte Carlo simulation on the combined forecasts and generate 1 million data points on each forecast series to estimate a triangular distribution; 2) take random samples from each of the simulated data sets and use the expected value with the highest frequency as the prediction. The forecast combinations are drawn from the following projections: Econoday.com’s consensus forecast data and the predictions generated by the models above. The forecasts are run in R with the “triangle” package.

Disclosure: None.

Comments

No Thumbs up yet!

No Thumbs up yet!