The Oil Situation: The SPR Is Being Raided To Close U.S. Production Deficit

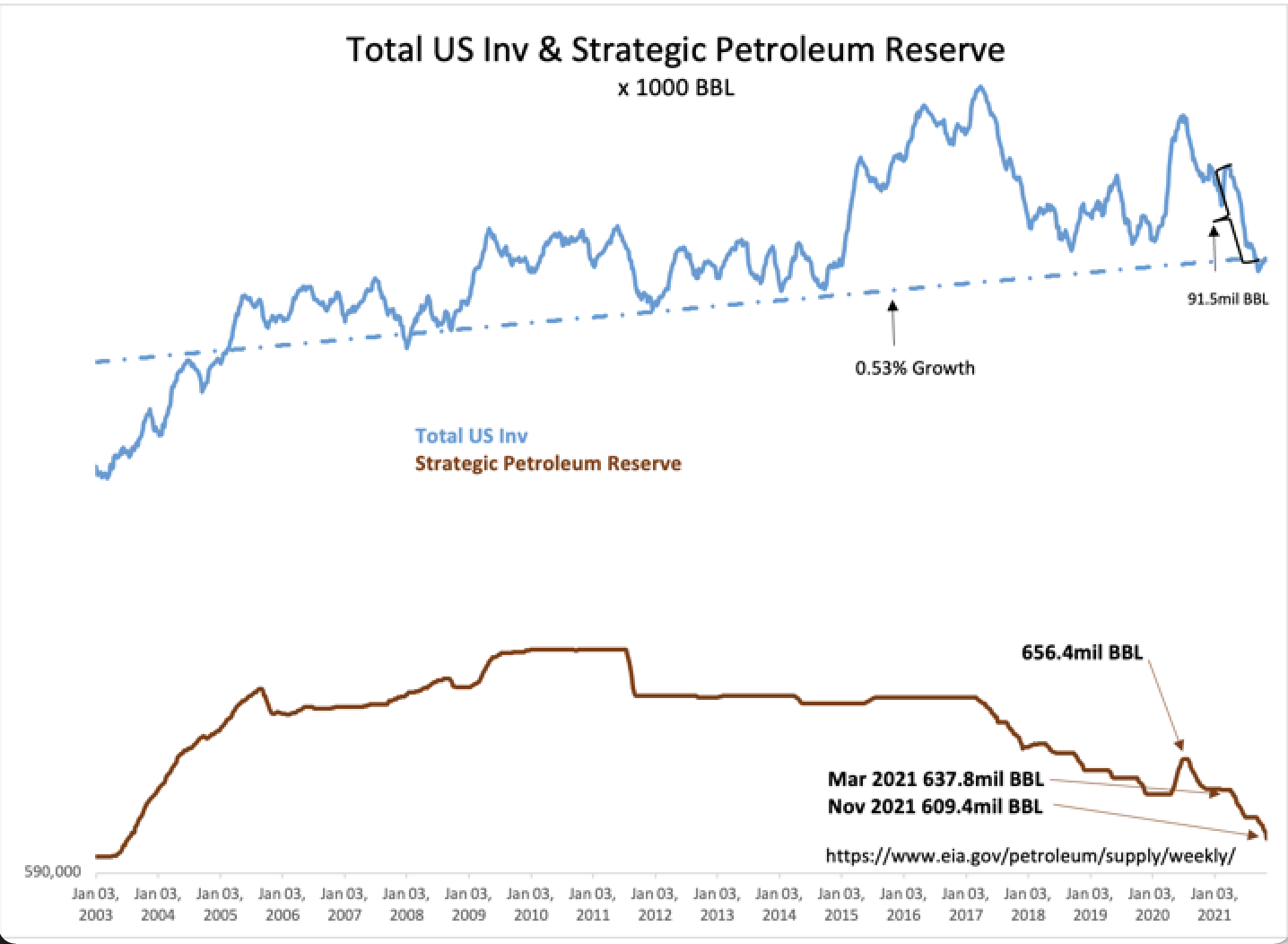

If the Total US Crude Inv including Strategic Petroleum Reserve(SPR), which is not routinely considered in the weekly commentary of crude inventory trends, is brought into consideration, the current deficit of US Crude Production suddenly looks very significant. Everyone is aware of the crude inventory declines as US normalizes post -COVID. This decline and the current level of US crude production of 11.5mil BBL/Day translate into a daily deficit vs consumption of 0.503mil BBL/Day once the declines of Total US Crude Inv(Total US Crude = weekly reported working US Crude Inv + Strategic Petroleum Reserve) are considered.

(Click on image to enlarge)

The Total US Inv has declined by 91.5mil BBL of crude oil since the end of Mar 2021. This is supply consumed but not supplied by US Crude Production which has varied either side of 11mil BBL/Day since Jun 2020 only recently rising to 11.5mil BBL/Day. Bringing the working inventory down to levels resulting in seeking greater profitability for the E&P industry is a necessary rebalancing post-COVID. The lowering of the SPR and throwing more crude into the system slows the return to profitability but is viewed as more a political benefit to slow the rise in energy prices as a result of government restriction on fossil fuel production.

(Click on image to enlarge)

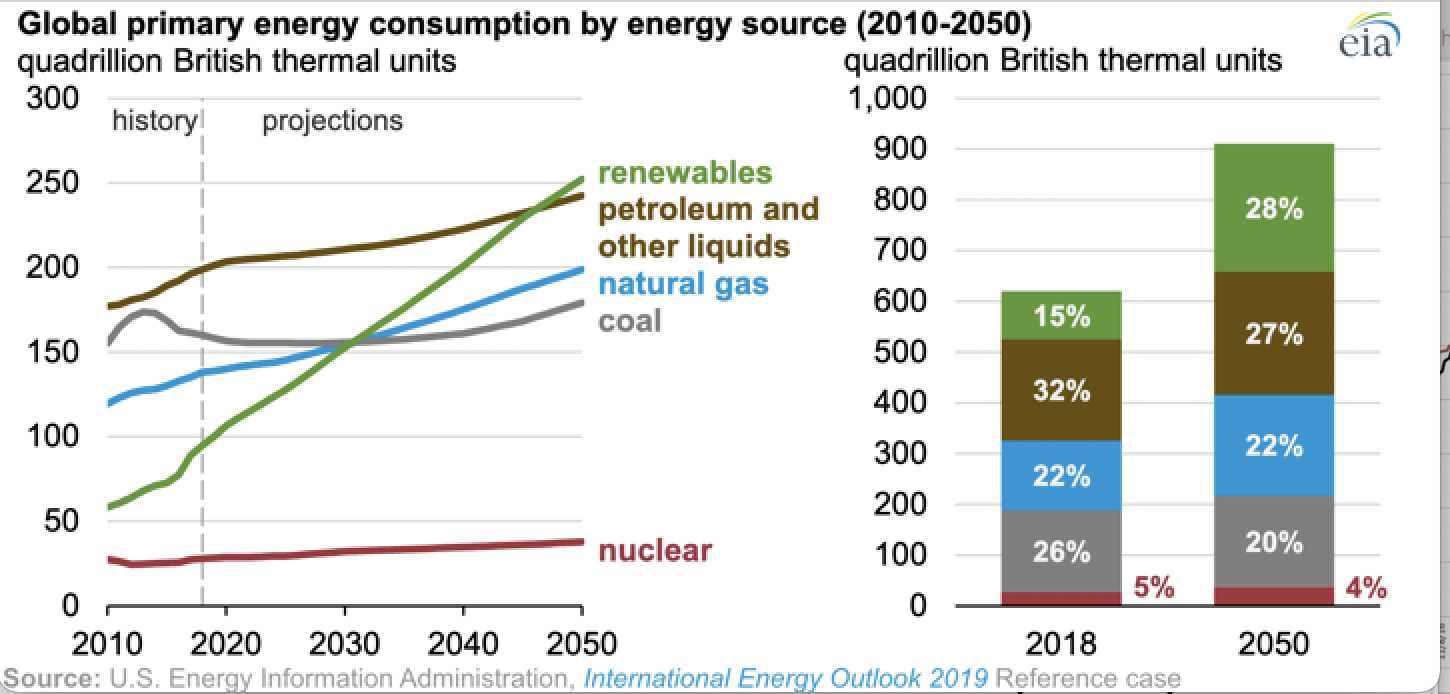

Where things go from here short-term is dependent on government policy. The long-term is dependent on global desires to maintain standards of living. Recent projections by the EIA expect a rise in the consumption of fossil fuels globally even as governments support alternative energy sources. The experiences of Texas with alternative sources and sudden cold weather and Europe with policies that have already replaced fossil fuel with renewable sources have forced all to reconsider these efforts. Energy production from wind and solar has proven unreliable when most needed during severe weather. There has already been a run on fossil fuels globally to offset some of the renewables as populations and economies have suffered.

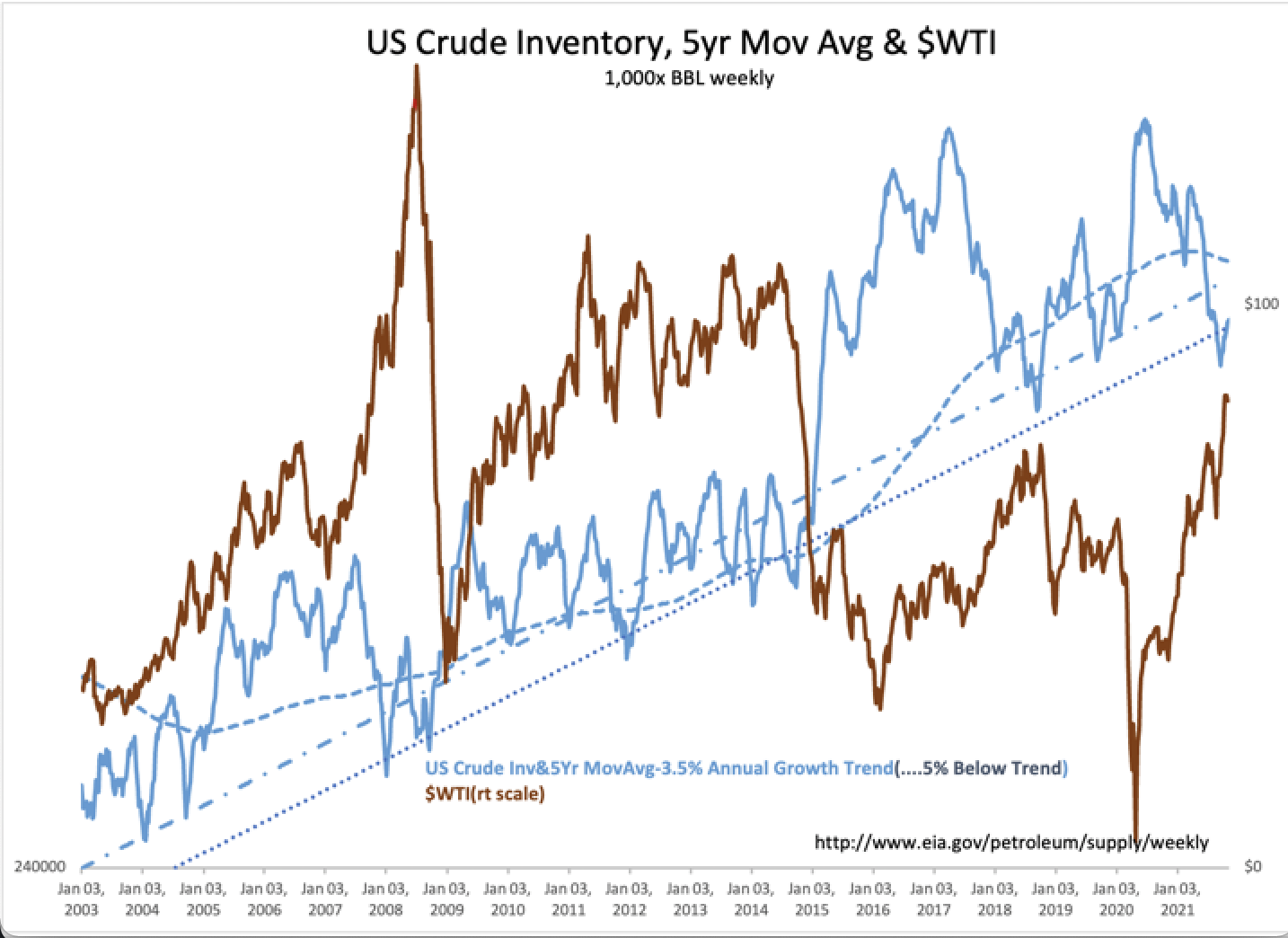

It is likely the transition away from fossil fuels will proceed more slowly. The US EIA crude inventory data reveal the US working inventory growth rate is 3.5% from a combination of domestic consumption and exports of refined products. The SPR is back to June 2003 levels with the recent decline. Additional SPR releases will only slow the rebalancing of the fossil fuel markets. Sooner rather than later, global demand will return with growth in consumption. The current decline in production cannot continue as at some point the US working inventory currently at historic lows will have to rise. The SPR cannot be used indefinitely to reflate working inventories.

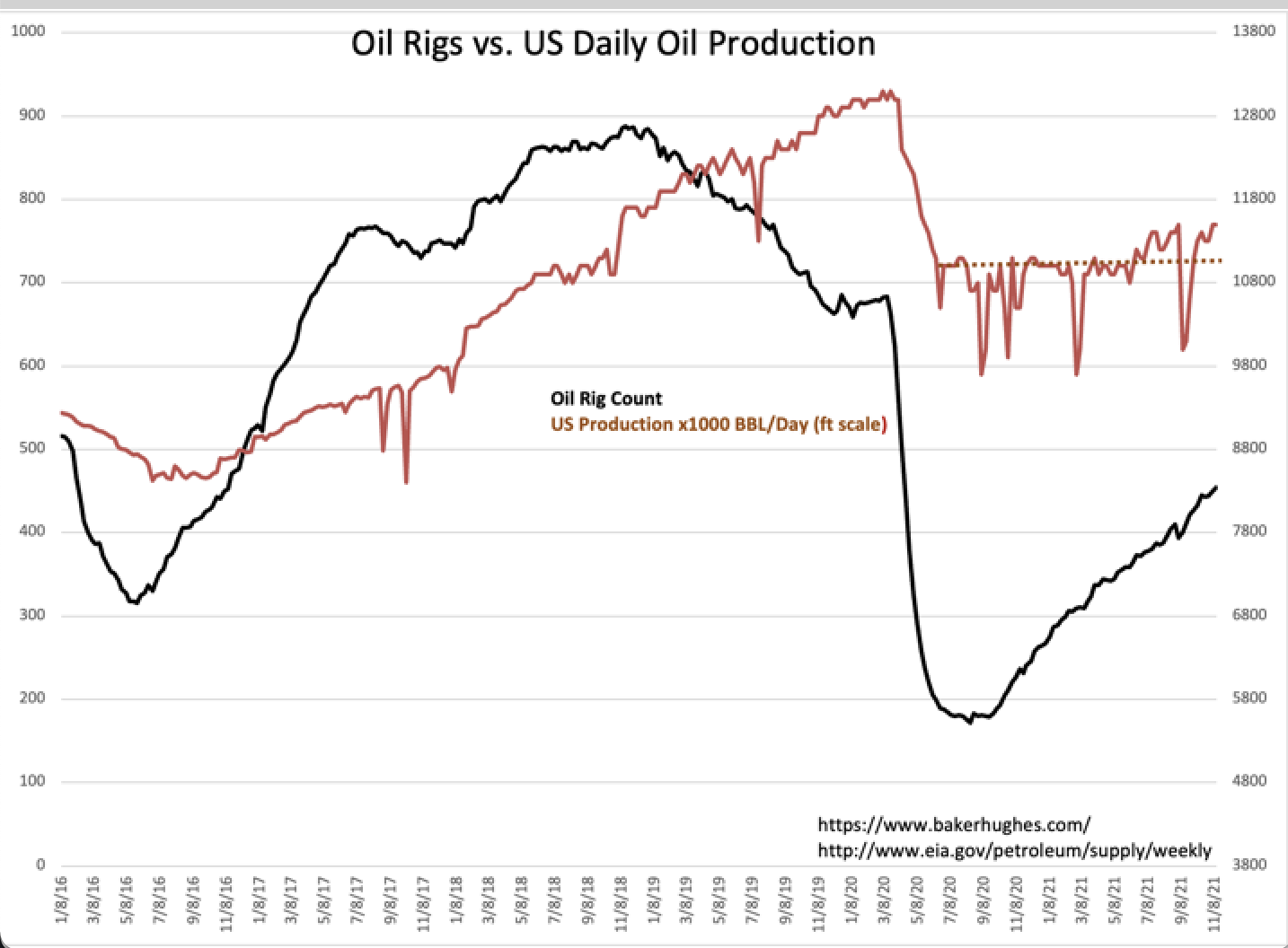

All indicators are signaling a global reopening post-COVID. Likewise, crude production indicators signal a cautious approach towards CAPEX focused production increases due to uncertainty in government policies. In my estimation, there will come a point when it is obvious the current undersupply cannot be offset by letting inventories fall further. The current administration may be in the early stages of recognition of this fact with multiple requests to foreign producers to increase supply. It may prove a hard turning point considering the political agenda to eliminate the petroleum industry.

Disclaimer: Riki nema disclaimer.

Comments

No Thumbs up yet!

No Thumbs up yet!